Introduction

You went to law school to practice law—not to reconcile client ledgers or fix QuickBooks errors at midnight before your CPA appointment. Yet here you are, dealing with financial pressure points that go far beyond typical small business bookkeeping:

- State bar compliance audits and IOLTA account requirements that carry ethics violations if mishandled

- Client billing disputes over untracked cost advances

- Year-end tax chaos when your general ledger doesn't separate earned income from client trust funds

This guide covers what online bookkeeping actually means for small law firms. Specifically, you'll find:

- Which bookkeeping tasks differ from other service businesses—and why they matter more

- Tools and services available, from legal-specific software like LeanLaw and CosmoLex to professional bookkeeping providers

- How to choose the right approach, whether you're handling it yourself, hiring out, or combining both

Key Takeaways

- Law firms must maintain two separate ledgers—operating accounts and IOLTA trust accounts—with three-way reconciliation required by most state bars

- Generic QuickBooks has no native trust account safeguards; 83% of California firms audited had noncompliant reconciliations

- The average firm carries 93 days of revenue in unbilled work and unpaid invoices, a direct cash flow drain

- Expect to pay $600–$1,500/month for legal bookkeeping vs. $300–$500 for general business bookkeeping

- Trust account violations drive 23% of California State Bar disciplinary cases—clean books are a license issue, not just a finance issue

Why Law Firm Bookkeeping Has Unique Requirements

The Dual-Ledger Reality: Operating and Trust Accounts

Law firms operate under financial requirements that most small businesses never encounter. You must maintain completely separate operating accounts (where your firm's earned income lives) and client trust accounts (IOLTA accounts holding unearned client funds). This isn't just best practice—it's an ethical and legal mandate. Commingling these funds triggers state bar investigations and can result in license suspensions. In California alone, 23% of all State Bar disciplinary cases from 2010-2021 involved client trust account allegations.

That's why bookkeeping at a law firm carries a compliance weight that most small businesses simply don't face.

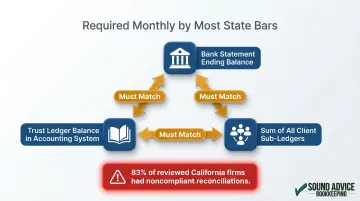

Trust Accounting: The Three-Way Reconciliation Requirement

Trust accounting means that unearned client funds—retainers, settlement proceeds awaiting distribution, advance deposits for case costs—must be held in trust and only transferred to your operating account once earned or approved.

The cornerstone of compliant trust accounting is the three-way reconciliation, which most states require monthly:

- Bank statement ending balance for the trust account

- Trust ledger balance in your accounting system

- Sum of all individual client sub-ledgers showing what you're holding for each client

These three numbers must match perfectly. Arizona, Florida, and California explicitly require monthly three-way reconciliations, and failure to perform them is the primary trigger for bar audits. In California's 2024 voluntary audit pilot, 83% of reviewed firms had noncompliant three-way reconciliations.

Legal Billing Complexity Reduces Revenue Recovery

Unlike straightforward service businesses, law firms juggle multiple billing arrangements within a single case—hourly rates, flat fees, contingency agreements, and split billing between matters. Each requires granular expense and time tracking.

When you fail to properly categorize a $350 filing fee as a client cost advance (instead of firm overhead), you absorb that cost rather than billing it back. Multiply that across dozens of matters, and the revenue loss compounds fast.

The median law firm in 2025 has 93 days of annual revenue trapped in "lockup": 43 days of unbilled work sitting in time entries that haven't been invoiced, plus 32 days of unpaid invoices waiting for client payment. This revenue leakage stems directly from poor bookkeeping and billing discipline.

State Bar Rules and ABA Model Rule 1.15

ABA Model Rule 1.15 (Safekeeping Property) establishes the foundational requirement: lawyers must hold client property separate from the lawyer's own property, maintain complete records, preserve those records for five years after representation ends, and promptly notify clients when funds are received or owed.

State bar rules build on this foundation with jurisdiction-specific requirements—meaning your bookkeeping system must adapt to your state's rules. IOLTA programs are mandatory in 47 jurisdictions, while 5 allow opt-out and 1 (Virgin Islands) is voluntary.

Solo Practitioners and Small Firms Lack Financial Oversight

Unlike larger firms with dedicated finance personnel, solo practitioners and small law firms typically lack someone whose job is to catch bookkeeping errors. Survey data shows that 45% of solo and small firm time is spent on administrative tasks—not practicing law.

Without a system in place from day one, errors accumulate quietly—often undetected until a bar audit or tax deadline surfaces months of compounded mistakes at once.

The Core Bookkeeping Tasks Small Law Firms Must Manage

Chart of Accounts Setup

Your chart of accounts is the backbone of your bookkeeping system—the categorization structure that organizes every transaction. Law firms need a legal-specific chart of accounts that separates:

- Operating income (earned legal fees)

- Trust liabilities (unearned client funds you're holding)

- Client cost advances (filing fees, expert witnesses, court costs you'll bill back)

- Firm expenses (rent, software, salaries, marketing)

Using a generic small business chart of accounts creates compliance gaps and gaps that obscure your true financial position. You need trust liability accounts that reflect your duty to hold client funds separately, plus sub-accounts tracking each client's individual balance.

Trust Account Management and Three-Way Reconciliation

Every month, without exception, you must complete the three-way trust reconciliation process:

Step 1: Reconcile your trust bank account statement to your trust ledger in QuickBooks (or your accounting software).

Step 2: Generate a report showing each individual client's trust balance from your client sub-ledgers.

Step 3: Verify that the total of all client sub-ledgers equals your trust ledger balance, which equals your bank statement ending balance.

If these three numbers don't match, you have a problem—either a recording error, a client ledger that went negative (meaning you spent Client A's money on Client B's costs), or missing transactions.

Most state bar investigations begin with reconciliation failures, not intentional theft. One Florida attorney was disciplined after failing to reconcile correctly, resulting in a $290,000 shortage.

Accounts Receivable and Collections Tracking

The bookkeeping workflow for client billing includes:

- Sending invoices for completed work and tracking whether they've been paid

- Drawing earned fees from trust into your operating account at the right time

- Outstanding balances (what clients owe you)

- Write-offs (uncollectible amounts you remove from AR)

Tracking your realization rate—what you billed versus what you actually collected—is a key profitability metric. The average law firm realization rate in 2025 is 88%, meaning 12% of billable work never gets invoiced. Your collection rate is 93%, meaning 7% of invoiced work never gets paid.

Expense Tracking and Cost Recovery

There's a critical distinction between:

- Firm overhead expenses (software subscriptions, rent, staff salaries, marketing)—these are your costs of doing business

- Client cost advances (filing fees, court reporter fees, expert witness charges)—these are costs you pay on behalf of the client and must bill back

Misclassifying client costs as firm overhead means you absorb expenses that should be recovered, directly eroding your margins. To prevent that, your bookkeeping system must track client cost advances separately and tie them to specific matters for billing purposes.

Bank Reconciliation and Financial Reporting

Beyond trust accounts, you must reconcile your operating account monthly—matching your bank statement to your accounting records to catch errors, unauthorized charges, or missing deposits.

The financial reports that matter most to small law firms:

- Profit & Loss (P&L): Shows revenue minus expenses for a period

- Cash Flow Statement: Tracks actual cash in and out (critical since you can be profitable on paper but cash-poor in reality)

- Accounts Receivable Aging: Shows how long invoices have been outstanding (30 days, 60 days, 90+ days)

These reports reveal your firm's true financial health and inform decisions about hiring, marketing spend, and case selection.

Online Bookkeeping for Law Firms: Tools, Services, or Both?

You have two primary paths—or a combination of both:

Path 1: Use legal-specific or general accounting software (QuickBooks Online with LeanLaw, CosmoLex, Clio Accounting) to manage bookkeeping in-house.

Path 2: Engage an online bookkeeping service where experienced professionals handle the books remotely.

Many firms benefit from combining professional bookkeeping services with robust software platforms.

The Software-Only Approach: Capabilities and Limitations

Tools like QuickBooks Online (when paired with legal add-ons like LeanLaw) or all-in-one platforms like Clio or CosmoLex can automate processes:

- Bank feeds automatically import transactions

- Client trust ledgers track individual balances

- Three-way reconciliation reports are generated automatically

- Trust-to-operating transfers are recorded with proper journal entries

But software has limitations: It doesn't catch categorization errors (coding a client cost as firm overhead), interpret compliance issues specific to your state bar rules, or provide strategic financial guidance. Standard QuickBooks Online lacks built-in safeguards that prevent you from overdrawing a client trust ledger or accidentally commingling funds.

Even legal-specific platforms include disclaimers. LeanLaw's terms state the software is provided "AS IS" without warranties, and CosmoLex notes it's not a law firm and use of the site doesn't constitute legal advice. Under ABA Model Rule 1.15, you retain personal, non-delegable responsibility for client funds—software can assist, but it doesn't assume liability.

The Online Bookkeeping Service Model

Professional bookkeeping services work remotely with law firm clients, maintaining books in real time using cloud tools. This is ideal for attorneys who want accurate books without becoming accounting experts.

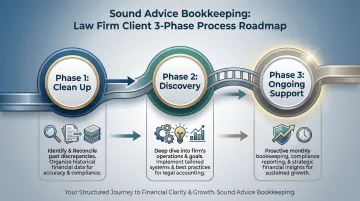

Sound Advice Bookkeeping serves small law firms and professional services clients across 30+ states, with a team bringing 100+ years of combined QuickBooks expertise. Flat-fee monthly pricing starts at $170/month based on transaction volume. Their 3-Phase Process is structured to address the specific scenarios law firms face:

- Phase 1 — Clean Up/Catch Up/Set Up ($85/hour): Corrects existing errors, catches up backlogged records, or builds clean systems from scratch—critical when trust accounts have gone unreconciled for months.

- Phase 2 — 3-Month Discovery Period ($85/hour): Analyzes transaction patterns, trust account complexity, and billing arrangements to set the right ongoing service level.

- Phase 3 — Ongoing Support (flat monthly fee): Covers reconciliation, monthly reporting, and compliance oversight at a predictable cost determined by Phase 2 findings.

For attorneys who want clean books and compliance confidence without a full-time hire, this structure delivers both.

When Each Option Makes Sense

Choose software-only if:

- You're a solo practitioner with simple finances (few trust clients, low transaction volume)

- You have time and aptitude to learn legal accounting principles

- You're willing to accept responsibility for categorization and compliance

Choose professional bookkeeping if:

- You're growing and handling multiple trust accounts

- You face complex billing arrangements across different practice areas

- You're under regulatory scrutiny or preparing for potential bar audits

- You want to focus on practicing law, not managing QuickBooks

Setting Up a Clean Bookkeeping System for Your Law Firm

Foundational Setup Steps

Get these four building blocks right before you touch a single transaction:

- Separate bank accounts — Maintain distinct operating and trust accounts. If your state requires it, open an IOLTA account at an approved financial institution. Commingling funds is a bar complaint waiting to happen.

- Legal-specific chart of accounts — Skip QuickBooks' default small business template. Build accounts that track trust liabilities, operating income by practice area, client cost advances, and firm overhead separately.

- The right accounting method — Most small law firms use cash basis accounting (income recorded when received, expenses when paid). Confirm with your CPA which method fits your tax strategy.

- A defined monthly close calendar — Set a hard deadline, such as the 10th of each month, to complete bank reconciliations, trust account three-way reconciliation, AR review, and financial statements.

Document Management and Receipt Tracking

Every transaction needs supporting documentation — especially client cost advances you'll bill back. Implement a workflow:

- Scan receipts immediately using mobile apps (HubDoc, Dext, or QuickBooks' built-in receipt capture)

- Store documents in organized folders (Google Drive, Dropbox) with clear naming conventions

- Link receipts to transactions in your accounting software

- Maintain this discipline monthly, not annually when preparing for taxes

Cloud-based tools make this manageable from anywhere, whether you're at the courthouse, a client site, or your home office.

That documentation discipline only works when it's tied to a consistent cadence. Here's the minimum rhythm every small law firm needs:

Minimum Monthly Bookkeeping Cadence

| Frequency | Task |

|---|---|

| Weekly | Categorize bank feed transactions in QuickBooks |

| Monthly | Reconcile operating and trust bank accounts |

| Monthly | Complete three-way trust reconciliation |

| Monthly | Review accounts receivable aging report |

| Monthly | Generate P&L and cash flow statements |

| Monthly | 30-minute financial review — cash position, outstanding AR, upcoming expenses, profitability trends |

Common Bookkeeping Mistakes Small Law Firms Make

Commingling Personal and Business Funds—or Operating and Trust Funds

Paying personal expenses from your business account creates tax headaches. Paying firm expenses from your trust account violates ethics rules and triggers bar complaints. Both mistakes are avoidable — and both are surprisingly common.

The solution is simple: maintain completely separate accounts with clear boundaries. Never write a check from trust to cover firm payroll, rent, or software subscriptions. Transfer only earned fees (after work is performed and documented) from trust to operating.

Neglecting to Reconcile Trust Accounts Monthly

Even when balances appear correct at the bank level, unreconciled trust accounts mask client ledger discrepancies that compound over time. The total balance in trust can look correct while Client A's sub-ledger is negative $500 and Client B's is overstated by $500 — meaning you used one client's money for another's expenses.

Most state bar investigations begin with reconciliation failures. In New Jersey's 2024 random audit program, 744 audits were conducted, and 98.5% of firms accounted for funds honestly — but 1.5% had serious ethics violations, and 16 attorneys were disciplined based solely on audit detection.

Misclassifying Expenses and Failing to Track Billable Client Costs

Attorneys frequently absorb client costs by failing to record them as cost advances. Common examples include:

- Court filing fees

- Expert witness costs

- Deposition expenses

- Process server charges

Instead of tracking these per client, they get categorized as firm expenses — or never recorded at all.

Every untracked cost reduces your profitability directly. A $500 expert witness fee misclassified as a firm expense is $500 you'll never recover from the client.

Multiply that across dozens of cases annually and you're leaving tens of thousands of dollars on the table — costs you already paid but can't bill back because there's no record of which client they belong to.

How to Choose the Right Online Bookkeeping Solution for Your Law Firm

Key Evaluation Criteria

- Legal/IOLTA compliance knowledge: Do they understand trust accounting rules, three-way reconciliation, and state bar compliance — not just in theory, but in practice?

- Law firm experience: Have they worked with attorneys before? Can they handle hourly billing, flat fees, contingency arrangements, and retainer draws?

- Platform familiarity: Are they fluent in QuickBooks? Do they know legal-specific tools like LeanLaw or practice management platforms like Clio?

- Pricing model: Hourly billing creates unpredictable costs. Flat monthly fees don't. Ask how the fee is determined — by transaction volume, trust client count, or time estimates.

- Strategic partner vs. data-entry vendor: Will they flag problems and offer guidance, or just process transactions and disappear until next month?

Questions to Ask Prospective Bookkeeping Services or Software Vendors

- "Can you handle three-way trust reconciliation monthly?" Hesitation or "We can try" is your answer. Move on.

- "How do you handle state bar audit requests?" You need to know what documentation they can produce — and how fast.

- "Do you have experience with retainer management, client cost advances, and split billing?" Generic bookkeeping experience doesn't automatically translate to legal accounting.

- "What does onboarding look like?" Get specifics: timeline, deliverables, and cost for getting your books clean and compliant.

- "What if our books are currently a mess?" This reveals whether they can remediate problems or only maintain books that are already clean.

Sound Advice Bookkeeping's Approach to Law Firm Clients

Sound Advice Bookkeeping's 3-Phase Process is built for small firms that need clean books and budget certainty without the cost of a full-time hire:

Phase 1 addresses the reality that many firms come to them with disorganized records—months of unreconciled transactions, missing documentation, or trust accounts that haven't been properly maintained. This cleanup is billed at $85/hour and establishes the foundation for ongoing compliance.

Phase 2 involves a 3-month discovery period (also $85/hour) where the team analyzes your specific transaction patterns, trust account complexity, and operational needs to determine the right ongoing service level and flat fee.

Phase 3 provides predictable, ongoing monthly management at a flat fee based on transaction volume—not hours worked. This gives you budget certainty while ensuring continuous compliance oversight.

With clients in 30+ states and 100+ years of combined bookkeeping and QuickBooks expertise, Sound Advice serves law firms and professional services practices that need more than software—they need experienced professionals who understand the stakes of trust account compliance.

Frequently Asked Questions

What is the difference between bookkeeping and accounting for a law firm?

Bookkeeping is the daily and monthly recording and categorization of transactions—entering deposits, coding expenses, reconciling bank accounts, and maintaining client trust ledgers. Accounting involves interpreting that data for tax preparation, financial analysis, and strategic planning. Errors in bookkeeping cascade directly into compliance problems and inaccurate tax filings, so both must be handled correctly.

Do small law firms need a dedicated bookkeeper?

Yes. Trust accounting compliance and bar discipline risk make professional bookkeeping support essential for most small firms. Online services like Sound Advice Bookkeeping provide expertise and compliance oversight at predictable monthly costs—a practical alternative to hiring in-house staff.

What is IOLTA and why does it matter for law firm bookkeeping?

IOLTA stands for Interest on Lawyers' Trust Accounts—special bank accounts where attorneys hold client funds that are nominal in amount or held for short periods. State bar rules require these accounts, and the interest generated funds civil legal services for indigent persons. Failing to track and reconcile IOLTA accounts properly is one of the most common causes of bar complaints and disciplinary action.

Can I use QuickBooks for law firm bookkeeping?

Yes, QuickBooks Online is widely used in law firm bookkeeping, particularly when paired with legal-specific add-ons like LeanLaw that automate trust accounting and three-way reconciliation. However, proper legal configuration and trust accounting setup are essential—ideally handled by a bookkeeper with law firm experience, as generic QuickBooks lacks native safeguards against trust account overdrafts or commingling.

How much does online bookkeeping for a small law firm cost?

Three major risks follow from inaccurate books:

- State bar discipline for trust account violations, up to license suspension or disbarment

- Missed revenue from untracked billable costs you absorb rather than recover from clients

- Poor decisions driven by bad data—overhiring, missing cash flow problems, or misjudging case profitability