Introduction

You're profitable on paper. The revenue numbers look good, clients are paying, and growth is happening—yet you're constantly stressed about cash. You check your bank balance before every purchase, delay vendor payments, and wonder if you can afford that new hire. The problem isn't your business model. It's that you're running your business from your checking account balance rather than from your books.

For most entrepreneurs, bookkeeping feels like administrative drudgery—something that pulls you away from building products, closing deals, and serving customers. But your books are the most powerful clarity tool you have. When they're accurate and current, you stop guessing and start making decisions based on what's actually happening in your business.

This guide walks you through building a bookkeeping system that actually serves your business—from day-one setup and key financial terms to common pitfalls, tracking cadences, and when to bring in professional help.

Key Takeaways

- Separate business and personal finances immediately to protect accuracy and limit legal liability

- Choose cash or accrual accounting based on your business model and stick to it consistently

- Establish a regular bookkeeping cadence: daily receipt capture, weekly transaction review, monthly reconciliation

- Hire professional help when books fall behind, admin consumes 20+ hours weekly, or tax complexity increases

Why Bookkeeping Is Non-Negotiable for Entrepreneurs

Bookkeeping isn't just about tax compliance or satisfying the IRS. It's about trading fear for informed certainty. Without accurate financial records, every business decision—whether to hire that salesperson, increase marketing spend, or take on debt—is made on gut feel rather than data.

The stakes are real. According to CB Insights analysis of 431 VC-backed startup post-mortems, 70% of failed startups cited "ran out of cash" as the ultimate cause of death. A 2025 QuickBooks survey found that 43% of small business owners say cash flow is a problem for their business. Running out of money doesn't happen suddenly—it happens slowly, invisibly, when you're not tracking the numbers that matter.

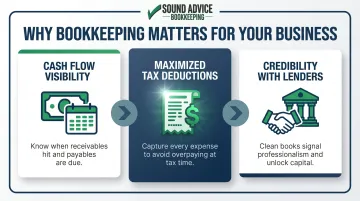

Good bookkeeping protects and grows your business in three concrete ways:

- Cash flow visibility: You always know when receivables will hit, when payables are due, and whether you can afford that next investment.

- Maximized tax deductions: Every legitimate expense is captured and categorized, so you're not overpaying at tax time. Lost receipts alone can cost entrepreneurs thousands annually.

- Credibility with lenders and investors: Banks and investors don't fund businesses with messy books. Clean financial statements signal professionalism and make capital accessible when you need it.

Bookkeeping vs. Accounting: Understanding the Division of Labor

Many entrepreneurs use "bookkeeping" and "accounting" interchangeably, but they serve different purposes. Bookkeeping is the day-to-day work: logging sales, categorizing expenses, reconciling bank statements. It keeps your financial records current and accurate.

Accounting builds on top of that data. Accountants analyze your books to prepare tax returns, generate financial reports, and advise on strategy—helping you understand what the numbers actually mean for your business.

Both matter, but bookkeeping is the foundation. Without clean transaction records, even the best accountant is working blind.

Setting Up Your Bookkeeping System From Day One

Your bookkeeping system is only as useful as the foundation it's built on. Get the structure right from day one, and you'll spend far less time untangling mistakes later.

Separate Personal and Business Finances Immediately

The most important first move is separating personal and business finances completely. Open a dedicated business bank account and business credit card, and use them exclusively for business transactions. Never mix personal and business expenses.

Commingling funds is the #1 bookkeeping error entrepreneurs make. A 2025 QuickBooks survey revealed that 7 in 10 small business owners have used a personal credit card to pay for business-related costs. This practice creates serious problems:

- Inaccurate profit calculations — When personal and business expenses mix, you can't determine true business profitability

- Missed tax deductions — Business expenses paid from personal accounts are often forgotten at tax time

- Legal liability exposure — For LLCs and corporations, commingling can "pierce the corporate veil," exposing your personal assets to business liabilities

Set up separate accounts from day one. It's the single easiest way to keep your books clean and your liability protection intact.

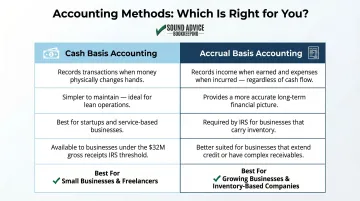

Choose Your Accounting Method: Cash vs. Accrual

The IRS recognizes two primary accounting methods, and you must choose one and apply it consistently.

Cash Basis Accounting:

- Records transactions when money actually changes hands

- Income reported when received; expenses deducted when paid

- Simpler to understand and maintain

- Good for most startups and service-based businesses

- Available if average annual gross receipts are under $32 million (2026 threshold)

Accrual Basis Accounting:

- Records income when earned and expenses when incurred, regardless of payment timing

- Provides more accurate picture of profitability over time

- Required if you carry inventory or when average gross receipts exceed $32 million

- Better for businesses that extend customer credit or carry significant receivables

Most early-stage businesses do best with cash basis — it's simpler and meets the needs of the majority of startups. The exception: if you carry inventory, offer customer credit terms, or operate in manufacturing, distribution, or food service, accrual accounting gives you a more accurate financial picture.

If your business later crosses the IRS revenue threshold or your financial complexity grows, consult a professional before switching methods. Sound Advice Bookkeeping has guided clients through this transition since 2009, using a structured setup process that keeps records accurate and compliant through the change.

Set Up Your Chart of Accounts

The chart of accounts is your categorized list of every type of transaction your business makes. It organizes your financial life into logical buckets that make reporting and analysis possible.

Start simple with five main categories:

- Assets — What you own (cash, equipment, accounts receivable)

- Liabilities — What you owe (loans, credit card balances, accounts payable)

- Equity — Your ownership stake in the business

- Revenue — Income from sales and services

- Expenses — Costs of running the business

Within each category, create subcategories as needed—but resist the urge to over-categorize at launch. Starting with 30 expense categories when you only have 10 types of expenses makes bookkeeping harder, not easier. You can always add accounts as your business grows and complexity increases.

Single-Entry vs. Double-Entry Bookkeeping

Single-entry bookkeeping works like a checkbook register: you record income and expenses in one place. It's simple and sufficient for very small businesses or side hustles, but it has limitations—no built-in error checking, difficult to generate financial statements, and not accepted by most lenders or investors.

Double-entry bookkeeping records every transaction in at least two accounts: once as a debit and once as a credit. This creates a self-balancing system where total debits must equal total credits, providing built-in error detection and enabling professional financial reporting.

Double-entry is the standard for any business beyond a one-person side hustle. The good news: modern accounting software handles double-entry automatically. You simply record transactions, and the software manages the debits and credits behind the scenes.

Choose Your Bookkeeping Tools

Spreadsheets:

- Free and familiar

- Complete control over structure

- Severe limitations: error-prone, no automation, doesn't scale, time-consuming

Cloud-Based Accounting Software (QuickBooks Online, Xero, FreshBooks):

- Automates transaction import from bank feeds

- Handles double-entry bookkeeping automatically

- Generates professional financial reports instantly

- Simplifies tax preparation

- Accessible from anywhere

- Monthly subscription cost ($15-$50+ depending on features)

For any business with more than occasional transactions, cloud-based accounting software pays for itself in time savings and error reduction. QuickBooks Online is the most widely adopted platform, with extensive third-party integrations and broad accountant/bookkeeper familiarity.

If you're unsure which version fits your business, that's a common sticking point. Sound Advice Bookkeeping's team has 100+ combined years of QuickBooks expertise across Online, Desktop, and Enterprise — and they help clients pick the right version and configure it correctly before bad habits set in.

Your Ongoing Bookkeeping Cadence: Daily, Weekly, and Monthly Tasks

Bookkeeping isn't a one-time setup—it's a rhythm. The entrepreneurs who stay on top of their books do it in small, consistent increments rather than marathon catch-up sessions. Establish these habits early.

Daily Habit: Capture Receipts Immediately

Snap photos or scan receipts the moment you receive them. Small cash expenses are the most commonly lost deductions. Recording them in the moment takes seconds; recovering them later is often impossible.

Use your accounting software's mobile app or a dedicated receipt-scanning app that integrates with your bookkeeping system. Categorize the expense right away while the context is fresh—was that lunch with a vendor a business meal or a personal expense? You'll remember today, but not in three months.

Weekly Habit: Review and Categorize Transactions

Set aside 30-60 minutes each week to:

- Review imported transactions from bank and credit card feeds

- Categorize expenses correctly (software will learn your patterns over time)

- Check open invoices — Who owes you money? How many days outstanding?

- Verify upcoming bills — What vendor payments are due in the next 7-10 days?

This weekly check-in prevents accounts receivable from aging into collection problems.

According to the 2025 Intuit QuickBooks Small Business Late Payments Report, 56% of U.S. small businesses are owed money from unpaid invoices, averaging $17,500 per business—and 47% report invoices overdue by more than 30 days. Businesses heavily affected by late payments were 1.4 times more likely to face cash flow issues. Weekly AR review catches problems before they compound.

Monthly Habit: Bank Reconciliation

Bank reconciliation means comparing your bookkeeping records to your bank and credit card statements line by line to catch errors, duplicate entries, and unauthorized charges.

This monthly discipline is critical. According to the Association of Certified Fraud Examiners 2024 Report, occupational frauds detected "by accident" lasted an average of 18 months with a median loss of $110,000. In contrast, frauds detected through active account reconciliation were caught in 8 months—10 months faster—preventing tens of thousands in additional losses.

Schedule reconciliation on the same day each month—the first or last business day works well—so it becomes routine rather than something you squeeze in when you remember.

Track Accounts Receivable and Payable

Accounts Receivable (AR) — money customers owe you

Accounts Payable (AP) — money you owe vendors

These are the pulse of cash flow. A business can be profitable on paper while running out of real cash because of slow-paying clients. Track AR aging reports weekly so you know exactly who owes what and for how long. Follow up on invoices at 30, 60, and 90 days to maintain healthy cash flow.

Sound Advice Bookkeeping handles both AR and AP as part of their flat-fee monthly packages—covering invoice tracking, vendor payment processing, and proactive collections follow-up so entrepreneurs can focus on running the business rather than chasing payments.

Record Retention: What to Keep and How Long

The IRS requires keeping business records to support income and deductions. Retention requirements vary by record type:

| Record Type | Retention Period |

|---|---|

| General tax records (receipts, invoices, bank statements) | 3 years from filing date |

| Employment tax records (payroll records, tax filings) | 4 years after tax due or paid date |

| Records for omitted income (>25% of gross income) | 6 years |

| Worthless securities or bad debt deductions | 7 years |

What to keep: Receipts, invoices, bank statements, credit card statements, payroll records, contracts, loan documents, and tax returns.

How to store it: Cloud-based digital storage organized by year and category is both legally sound and audit-ready. Scan paper receipts and store them in organized folders within Google Drive, Dropbox, or directly in your accounting software.

Key Bookkeeping Terms Every Entrepreneur Should Know

Knowing basic accounting vocabulary makes your financials readable and puts you on equal footing with bookkeepers, accountants, and lenders.

The Accounting Equation

Assets = Liabilities + Equity

This fundamental equation keeps every set of books balanced. Everything your business owns (assets) is financed either by what you owe (liabilities) or what you've invested (equity).

- Assets — What you own: cash, equipment, inventory, accounts receivable

- Liabilities — What you owe: loans, credit card balances, accounts payable

- Equity — Your ownership stake after liabilities are subtracted from assets

These three components feed directly into your financial statements — the reports that show where your business actually stands.

Three Essential Financial Statements

Income Statement (Profit & Loss / P&L):

- Shows revenue minus expenses for a specific period (month, quarter, year)

- Answers: Did the business make or lose money?

- Critical for understanding profitability trends

Balance Sheet:

- Snapshot of financial position at a specific point in time

- Lists assets, liabilities, and equity

- Answers: What does the business own and owe right now?

Cash Flow Statement:

- Tracks where cash came from and where it went

- Categorizes cash movement: operating, investing, financing activities

- Essential for day-to-day decisions: a profitable business can still run out of cash

Additional Key Terms

- Cost of Goods Sold (COGS) — Direct costs tied to producing what you sell (materials, direct labor). Revenue minus COGS equals gross profit.

- General Ledger — The master record of all transactions, organized by account

- Accounts Payable (AP) — Money you owe vendors for goods/services received but not yet paid

- Accounts Receivable (AR) — Money customers owe you for goods/services delivered but not yet paid

Common Bookkeeping Mistakes That Cost Entrepreneurs

Even small errors compound over time. Avoid these common pitfalls.

Procrastinating on Entries

Letting transactions pile up is a slow drain. Receipts go missing, categorization becomes guesswork, and the quarterly catch-up session takes 10x longer than staying current ever would.

According to Cornerstone Advisors research, small business owners spend an average of 20 hours per week on accounting tasks, much of it on catch-up work that consistent weekly entries would have prevented.

The fix: Schedule a non-negotiable weekly bookkeeping appointment on your calendar. Treat it like a client meeting—it doesn't get moved or skipped.

Misclassifying Expenses

Putting expenses in the wrong category creates two problems:

- Financial reports become unreliable — You can't make informed decisions when your P&L is inaccurate

- Tax errors — You either miss legitimate deductions or claim deductions you're not entitled to, risking IRS penalties

Most commonly confused classifications:

- Capital expenditures vs. operating expenses — Equipment purchases over certain thresholds must be depreciated over time, not expensed immediately

- Owner's draw vs. salary — LLCs and partnerships typically use draws; corporations use salary. Each has different tax implications.

- Personal vs. business expenses — That "working lunch" alone at Chipotle is personal. Lunch with a client discussing business is deductible.

Misclassifying Workers: Employee vs. Independent Contractor

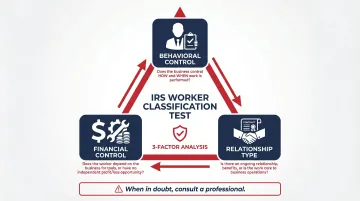

The IRS strictly enforces worker classification using a 3-factor common-law test:

- Behavioral Control — Does your business direct the method, schedule, and location of the work, not just the outcome?

- Financial Control — Does the worker depend on you for tools, reimbursements, or have no opportunity for independent profit or loss?

- Relationship Type — Is there an ongoing contract, employee benefits, or is this work central to your core business operations?

Misclassifying an employee as a contractor to avoid payroll taxes is one of the most heavily penalized bookkeeping errors. The Trust Fund Recovery Penalty (TFRP) holds responsible parties personally liable for unpaid payroll taxes — and intentional disregard can add failure-to-file penalties of up to $680 per return. If there's any ambiguity about a worker's status, get a professional opinion before it becomes a liability.

Should You DIY or Hire a Professional Bookkeeper?

Self-managed bookkeeping works when transaction volume is low and your business model is straightforward. It starts to break down when:

- Books fall consistently behind

- Financial admin is eating multiple hours each week

- Tax situations grow complex or unpredictable

Three Primary Options and Their Tradeoffs

| Option | Monthly Cost | Your Time | Best For |

|---|---|---|---|

| Full DIY with Software | $15–$50/mo | 15–25 hrs/week | Very early stage, simple finances |

| Outsourced Bookkeeper | $170–$750+/mo | 2–5 hrs/month | Growing businesses, owners who want time back |

| Full-Service Firm | $750–$1,250+/mo | Minimal | Complex financials, controller-level needs |

DIY carries the lowest dollar cost but the highest time and error risk. Professional options cost more upfront — and typically pay for themselves quickly.

The Real ROI of Professional Bookkeeping

Consider the time cost alone. If you're spending 25 hours per week on manual data entry and reconciliation, that's 100+ hours per month not spent on revenue-generating work.

At even a modest $100/hour opportunity cost, that's $10,000/month in lost productivity — far exceeding what professional bookkeeping costs.

That math changes the conversation. The question isn't whether you can afford a bookkeeper — it's whether you can afford not to have one.

Sound Advice Bookkeeping: Built for Entrepreneurs

Sound Advice Bookkeeping was created by small business owners who understand that bookkeeping should do more than satisfy the tax man — it should provide the clarity and confidence entrepreneurs need to grow.

Operating since 2007 and having serviced over 1,000 small businesses, Sound Advice approaches every engagement with growth and efficiency as the primary goals. Their unique 3-phase process produces customized flat-fee monthly packages starting at $170/month:

- Phase 1 (Clean Up/Catch Up/Set Up): Organize existing records, catch up on past work, or establish new systems from scratch

- Phase 2 (3-Month Discovery Period): Analyze your business operations and transaction patterns to determine appropriate ongoing support

- Phase 3 (Ongoing Support): Flat-fee monthly service based on transaction volume, not hours spent

With 100+ combined years of QuickBooks expertise, the team functions as an extension of your business. They're not just recording transactions — they're building the financial foundation you need to make confident decisions.

Frequently Asked Questions

What is the difference between bookkeeping and accounting?

Bookkeeping is the systematic recording of daily transactions—logging sales, categorizing expenses, reconciling accounts. Accounting involves interpreting that data to make strategic decisions, prepare taxes, and generate financial reports. Most small businesses need both, with bookkeeping providing the foundation for accounting analysis.

How often should I update my books as an entrepreneur?

Record transactions daily or at minimum weekly, reconcile accounts monthly, and review full financial reports quarterly. Staying current costs far less time than catching up. Weekly updates take 30-60 minutes; quarterly catch-ups can consume entire days.

Can I do my own bookkeeping without an accounting background?

Yes, especially with modern accounting software that automates much of the process. However, as transaction complexity grows, the risk of errors increases and the time cost rises—making professional help worth evaluating. Most entrepreneurs successfully DIY initially but transition to professional support as they scale.

What financial records do I need to keep for taxes?

Keep receipts, invoices, bank and credit card statements, payroll records, and contracts. IRS retention requirements vary by record type:

- Most business records: 3 years minimum

- Employment tax records: 4 years

- Worthless securities, bad debt deductions: 7 years

When should I switch from cash-basis to accrual accounting?

Switch when your business carries inventory, extends customer credit, seeks outside investment, or when average annual gross receipts cross the $32 million IRS threshold that mandates accrual accounting. Consult a professional before making the change to ensure proper implementation and compliance.

Bookkeeping stops feeling like a burden the moment you start using it as a decision-making tool. Your books reflect what's actually happening in your business—not what you assume. Kept current and understood clearly, they give you the confidence to act on facts rather than instincts.