Introduction

Most solopreneurs run their businesses by logging into their bank account to "check" if they can afford something. This reactive approach to financial management is dangerous—it ignores outstanding invoices, upcoming liabilities, and the real health of your business. Without consistent monthly bookkeeping, you're exposed to cash flow shortfalls and tax penalties that build quietly until they become urgent problems.

This guide delivers a repeatable monthly bookkeeping system built for solopreneurs. No finance degree required—just a practical framework to understand your numbers, make confident decisions, and stay tax-ready year-round.

Key Takeaways

- Monthly bookkeeping gives you financial visibility for smart decisions year-round — not just at tax time

- Build three rhythms: weekly 15-minute transaction reviews, mid-month check-ins, and month-end reconciliation

- Separate business and personal finances and set up cloud-based software before anything else

- Review your Profit & Loss, Cash Flow Statement, and Accounts Receivable Aging report every month

- If you're spending 5+ hours monthly on bookkeeping or consistently falling behind, it's time for professional help

Why Monthly Bookkeeping Matters More Than You Think

"Doing books at tax time" is the single most expensive bookkeeping mistake a solopreneur can make. In Fiscal Year 2024 alone, the IRS assessed $4.8 billion in estimated tax penalties across 15.3 million individual returns. Missed deductions, surprise tax bills, and cash flow blind spots accumulate throughout the year when you wait until April to organize your finances.

Monthly bookkeeping gives you a clear picture of income trends, expense patterns, and whether you're actually profitable — not just cash-positive. Those two things aren't the same. A business can show profit on paper while running out of cash to cover next month's bills. Catching that gap early is exactly what consistent monthly records make possible.

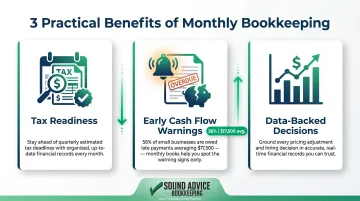

The Three Practical Benefits for Solopreneurs

Tracking your books each month delivers three concrete advantages:

- Tax readiness: Quarterly estimated tax planning gets easier when you know your numbers. You'll set aside the right amount each month instead of scrambling when payments are due.

- Early cash flow warnings: 56% of U.S. small businesses are owed money from late payments, averaging $17,500 per business. Monthly accounts receivable reviews let you follow up before debts become write-offs.

- Decisions backed by data: Accurate records let you evaluate pricing, decide when to bring in help, or invest in new tools — based on facts, not gut feeling.

Before You Start: The One-Time Setup for Your Monthly System

Separate Business and Personal Finances First

Mixing personal and business finances creates a categorization nightmare — and poses serious legal risks. For LLC owners, commingling funds is a primary trigger for "piercing the corporate veil" — the legal mechanism that strips away your personal asset protection. Courts scrutinize this directly when determining whether to hold owners personally liable for business debts.

Before anything else, open a dedicated business checking account and business credit card. Approximately 96% of small businesses maintain dedicated business bank accounts — this separation is standard practice for good reason.

Choose Cloud-Based Bookkeeping Software

Solopreneurs don't need enterprise accounting software — you need a cloud-based tool that auto-syncs with your bank account and payment processors to minimize manual data entry. Currently, QuickBooks holds 62% of the U.S. small business accounting software market, making it the industry standard.

If you're unsure which QuickBooks version fits your business — Online, Desktop, or Enterprise — working with an experienced bookkeeper during setup can save hours of trial-and-error reconfiguration later.

Set Up Your Chart of Accounts

Create categories relevant to your business before your first transaction. Common solopreneur expense categories include:

- Software subscriptions and digital tools

- Home office expenses

- Professional development and courses

- Contract labor and freelancers

- Marketing and advertising

- Business travel and meals

Proper categorization from day one makes monthly reviews and tax prep significantly faster while maximizing deductions.

Your Monthly Bookkeeping Checklist: A Week-by-Week Breakdown

The most effective monthly system isn't one big session at month-end—it's small, consistent actions spread across the month that take 15–30 minutes at a time.

Weeks 1–2: Weekly Transaction Review

Time Investment: 15 minutes weekly

Log into your accounting software and review all imported transactions from the past seven days. Each session, you're doing three things:

- Categorize anything that wasn't auto-categorized

- Match receipts to transactions using a receipt scanning app

- Flag any duplicates or errors before they compound

Catching miscategorizations weekly is far easier than untangling four weeks of errors at once. This habit is what separates solopreneurs who stay on top of their books from those who abandon the process entirely.

Week 3: Mid-Month Check-In

Time Investment: 30 minutes

Your mid-month review covers three critical areas:

- Accounts receivable: Identify overdue invoices and send reminders now. 47% of businesses report invoices more than 30 days overdue—every late payment is essentially an interest-free loan against your cash flow.

- Cash position: Compare current cash against expected expenses for the rest of the month. Are you on pace to hit your revenue target, or do you need to accelerate collections?

- Non-bank transactions: Document cash payments, reimbursements, or anything that won't auto-import from your bank feed.

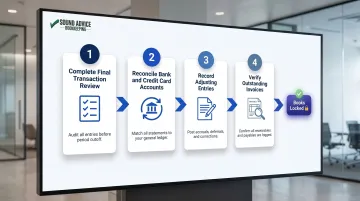

Week 4: Month-End Close

Time Investment: 45–60 minutes

The month-end close is your most important monthly task. Follow this sequence:

- Complete Final Transaction Review: Ensure every transaction from the month is recorded and categorized correctly

- Reconcile Bank and Credit Card Accounts: Confirm that every transaction in your accounting software matches your actual bank statement line by line. This catches errors, unauthorized charges, and sync failures before they compound

- Record Adjusting Entries: Document prepaid expenses or depreciation if applicable

- Verify Outstanding Invoices: Ensure all unpaid invoices are recorded and accurate

Once reconciliation is done, your books are locked for the month—and that's exactly the right moment to assess where you stand on quarterly taxes.

Quarterly Tax Awareness

The IRS requires quarterly estimated payments if you expect to owe at least $1,000 in tax after withholding and credits. Four deadlines to keep on your calendar:

- April 15

- June 15

- September 15

- January 15

Set aside a consistent percentage of net income each month so these payments don't hit as a financial shock. Most solopreneurs need to reserve 25–35% of net income for federal and state taxes combined.

The Financial Reports Every Solopreneur Should Pull Monthly

Pulling reports is only valuable if you know what you're looking for. These three reports answer the questions that matter most: Am I profitable? Do I have enough cash? Am I growing?

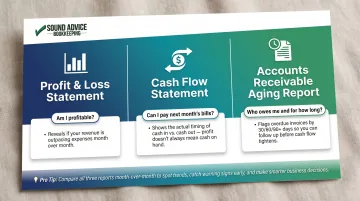

Profit & Loss Statement (P&L)

Your P&L shows revenue minus expenses — the net profit or loss for the month. When reviewing it, look for expense categories growing faster than revenue. If your software subscriptions increased 40% while revenue stayed flat, that's a red flag.

The P&L reveals whether your pricing covers your actual costs and where margin is quietly eroding.

Cash Flow Statement

You can be profitable on paper and still run short on cash. The difference between profit and cash flow comes down to timing: profit counts sales made on credit, while cash flow tracks what's actually hit your account — invoice collections, loan repayments, owner draws.

For solopreneurs with project-based or irregular income, this report is the one to watch most closely.

Accounts Receivable Aging Report

This report breaks outstanding invoices into buckets: current, 30, 60, or 90+ days overdue. It answers "who owes me and for how long" — which is exactly the information you need to follow up before unpaid invoices become write-offs.

The numbers back up why this matters: 43% of credit-based B2B sales for U.S. companies are currently overdue, with average payment terms sitting at 45 days.

Rather than reviewing each month in isolation, compare all three reports month-over-month. Patterns emerge that a single snapshot misses — seasonality, expense creep, and growth trends that should shape how you price, spend, and plan.

Common Monthly Bookkeeping Mistakes Solopreneurs Make

Letting Months Go Unreconciled

This is the #1 source of bookkeeping overwhelm. When you try to "catch up" after letting three, six, or twelve months go unreconciled, the cleanup cost in time or money almost always exceeds what consistent monthly upkeep would have cost. Cleanup bookkeeping typically costs $25–$50 per hour or $2,500–$5,000 flat, depending on severity.

Treating Your Bank Balance as Financial Health

Your checking account balance is misleading—it ignores outstanding invoices, upcoming liabilities, and unrecorded expenses. Your P&L tells you whether the business is profitable. Your cash flow statement tells you whether you can pay next month's bills. The number in your bank account tells you neither.

Skipping Bookkeeping During Busy Seasons

High-revenue months are exactly when bookkeeping errors are most likely and most expensive to miss. Automation keeps you consistent when time is tight:

- Set up auto-import so transactions flow in without manual entry

- Create recurring invoices for repeat clients

- Use scheduled reminders to flag your monthly close tasks

These three habits take an hour to configure and eliminate the most common busy-season gaps.

When It's Time to Stop DIYing Your Books

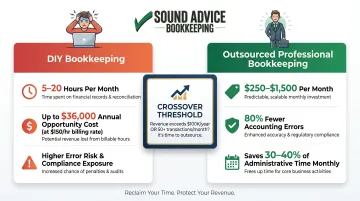

DIY bookkeeping makes sense for very simple operations, but it becomes a liability rather than a cost-saver when you cross certain thresholds. Small business owners spend 5 to 20 hours per month on bookkeeping—if you bill at $150/hour, this represents up to $36,000 annually in lost opportunity cost.

Signals You Need Professional Support

- Spending more than 5 hours per month on bookkeeping

- Falling consistently behind on reconciliation

- Facing multi-state tax obligations

- Needing clean financials for a loan or business decision

- Losing confidence in the accuracy of your numbers

The Cost-Benefit of Outsourcing

Professional outsourced bookkeeping for small businesses typically costs $250–$1,500 per month, far less than hiring an in-house bookkeeper ($60,000–$75,000+ annually including benefits). It becomes mathematically cheaper than DIY once your business crosses $100,000 in revenue or 50 transactions per month.

Professional bookkeeping also reduces accounting errors by 80% compared to non-specialist staff and saves 30–40% of administrative time monthly.

Those numbers are why solopreneurs increasingly turn to services like Sound Advice Bookkeeping, which offers flat-fee monthly packages starting at $170/month — priced by transaction volume, not time spent. The team works as an extension of your business, not a once-a-year tax contact. If your books are starting to feel like a burden, that's your signal. Call 303.228.8911 or schedule a consultation to explore monthly service options.

Frequently Asked Questions

What are the three golden rules of bookkeeping?

The three golden rules ensure every transaction is recorded accurately in double-entry bookkeeping:

- Personal accounts: Debit the receiver, credit the giver

- Real accounts: Debit what comes in, credit what goes out

- Nominal accounts: Debit all expenses/losses, credit all incomes/gains

How long does monthly bookkeeping take for a solopreneur?

With a solid system and automated tools, most solopreneurs maintain their books in 1–2 hours per month through short weekly sessions. Falling behind is what turns bookkeeping into a multi-hour ordeal—consistency is exponentially more efficient than catch-up work.

What financial reports should a solopreneur review each month?

Three reports cover the essentials: the Profit & Loss Statement, Cash Flow Statement, and Accounts Receivable Aging Report (who owes you money, and how long?). Each answers a distinct question your business needs to act on every month.

Should solopreneurs use cash basis or accrual accounting?

Most solopreneurs start with cash basis accounting — recording income when received and expenses when paid — because it's simpler to manage. Accrual accounting may become necessary as revenue grows. Per the IRS Publication 334, businesses averaging $31 million or less in annual gross receipts can use the cash method through 2025.

How do I catch up on bookkeeping if I'm several months behind?

Start with the oldest period and work forward, gathering all bank statements and receipts. For backlogs of 3+ months, hiring a professional bookkeeper for a cleanup engagement is often faster and more cost-effective than attempting it yourself. Sound Advice Bookkeeping's Phase 1 cleanup service addresses exactly this situation.

When should a solopreneur hire a bookkeeper?

Hire when you're spending more than 5 hours monthly on books, consistently falling behind, facing complex tax situations, or losing confidence in your numbers. The earlier you bring in support, the less cleanup you'll need — a bookkeeper caught early costs far less than one hired after the damage is done.