Introduction: Why SaaS Accounting Isn't Just Regular Bookkeeping

Picture this: Your SaaS startup just landed five annual subscriptions at $12,000 each. Your bank account shows $60,000 in fresh deposits. But here's the problem—you haven't actually earned that revenue yet. You've simply received payment for services you'll deliver over the next twelve months. This fundamental tension between cash received and revenue earned is what makes SaaS accounting its own discipline.

According to a CB Insights' 2026 analysis of 431 VC-backed companies that shut down since 2023, 70% ran out of capital. While capital depletion is often the final symptom, the underlying causes include poor product-market fit (43%), bad timing (29%), and unsustainable unit economics (19%).

The pattern across these failures is consistent: founders lacked the financial visibility to catch problems before they became fatal. Getting your accounting right from day one is a competitive survival advantage—not an administrative afterthought.

TLDR:

- SaaS accounting separates cash received from revenue earned—annual prepayments create deferred revenue liabilities

- Cash-basis accounting misleads founders by overstating profitability when large prepayments arrive

- Accrual accounting and GAAP compliance prevent costly corrections during fundraising and audits

- Tracking MRR, ARR, churn, and LTV:CAC is mandatory for investor conversations

- Professional bookkeeping support pays for itself by preventing compliance errors and creating investor-ready financials

What Makes SaaS Accounting Different from Traditional Bookkeeping

The Timing Gap That Changes Everything

Traditional businesses record revenue when a sale closes. A consulting firm invoices $10,000 for a completed project and recognizes $10,000 in revenue. Simple. SaaS companies operate under a completely different model: they earn revenue gradually as they deliver service over the subscription period. This creates a fundamental gap where cash in the bank and recognized revenue are often vastly different numbers.

Three Concepts Founders Must Track Separately

According to NetSuite's 2025 framework, SaaS businesses must separately track:

- Bookings: Total value of contracts signed (forward-looking indicator of growth)

- Billings: Amounts actually invoiced (primary cash flow indicator)

- Revenue: Amounts earned by delivering services under ASC 606 (actual income recognition)

Conflating these three metrics distorts financial statements. A founder who treats $60,000 in annual billings as $60,000 in monthly revenue will completely misread their business performance.

Why Cash-Basis Accounting Breaks Down for SaaS

Cash-basis accounting counts revenue when payment arrives. For SaaS companies receiving annual prepayments, this creates wildly misleading swings: months with large contracts look artificially profitable, while service-delivery months with few new sales appear weak. This roller-coaster view obscures the actual health of your recurring revenue engine.

The Cost Structure Advantage

That distortion matters even more when you factor in what SaaS margins actually look like. OpenView Partners' 2022 SaaS benchmarks show typical gross margins of:

- 70% for startups under $1M ARR

- 77% for $1M–$2.5M ARR

- 80% for $2.5M–$50M ARR

These margins—far higher than traditional product or service businesses—reflect lower direct costs of goods sold (hosting, support, infrastructure) relative to revenue. The path to profitability here isn't about cutting per-unit manufacturing costs. It's about scaling recurring revenue efficiently.

Different Metrics for a Different Model

Traditional businesses track gross profit margins and unit sales. SaaS businesses need a different set of gauges entirely:

- MRR / ARR: Monthly and annual recurring revenue — the pulse of your subscription engine

- Churn rate: The percentage of customers or revenue lost each period

- LTV:CAC ratio: Customer Lifetime Value versus Customer Acquisition Cost — the clearest signal of long-term viability

A standard P&L won't surface these signals. Building SaaS financial visibility means tracking these metrics alongside — not instead of — traditional statements.

Setting Up Your SaaS Accounting Foundation from Day One

Startups that skip GAAP-compliant practices or choose the wrong accounting method face painful, expensive corrections when seeking funding or preparing for audits. Setting up correctly from day one builds investor credibility and prevents the costly rework that derails so many early fundraising rounds.

Choosing Your Accounting Method

Accrual vs. Cash Basis for SaaS:

Accrual accounting counts revenue when it's earned—as you deliver the service—not when cash arrives. For a SaaS company billing annual subscriptions, this means spreading $12,000 received upfront across twelve monthly revenue entries of $1,000 each. Cash-basis accounting, by contrast, would incorrectly record the entire $12,000 in month one.

Accrual is the strongly preferred—and often required—method for SaaS companies because it accurately reflects subscription-based performance. Very early-stage startups sometimes start with cash accounting for simplicity, but plan to transition to accrual as soon as you begin taking subscription payments or seeking outside investment.

Investors, banks, and government regulators typically require accrual-based financials. Starting there saves you the painful process of restating historical records later.

Regulatory Reality:

Under IRS Revenue Procedure 2025-32, companies with 3-year average annual gross receipts exceeding $32 million (for taxable years beginning in 2026) must use accrual accounting and file Form 3115 to transition.

Building GAAP-Compliant Practices Early

GAAP (Generally Accepted Accounting Principles) provides standardized rules for financial reporting. While private early-stage startups aren't legally required to follow GAAP, adopting these practices early builds credibility with investors, simplifies fundraising due diligence, and prevents reporting errors that can derail an exit.

Practical First Steps:

- Open a dedicated business bank account, separate from personal finances

- Implement accounting software that handles recurring billing and deferred revenue—QuickBooks Online, Desktop, or Enterprise are well-suited for early-stage startups

- Establish a chart of accounts that separates deferred revenue, earned revenue, and recurring vs. non-recurring income

- Connect financial institutions to your accounting platform for automated transaction tracking

Getting these systems configured correctly from the start prevents the cleanup nightmares that eat time and money before a funding round. Sound Advice Bookkeeping has spent over 15 years helping startups build this foundation—with more than 100 combined years of QuickBooks expertise across the team.

Revenue Recognition and Deferred Revenue: The Core of SaaS Accounting

Revenue can only be "recognized"—counted as earned income—when your company has actually delivered the service promised. For a SaaS company, that means spreading a prepaid subscription payment across the service period, not recording it all at once.

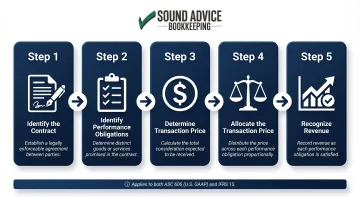

The Regulatory Framework: ASC 606 and IFRS 15

FASB ASC 606 (U.S. GAAP) and IFRS 15 (international) govern SaaS revenue recognition through a standardized five-step process:

- Identify the contract with a customer

- Identify performance obligations in the contract

- Determine the transaction price

- Allocate the price to performance obligations

- Recognize revenue as each obligation is satisfied

For SaaS subscriptions, revenue is typically recognized over time because customers simultaneously receive and consume benefits as you deliver the service.

A Concrete Example: The $12,000 Annual Subscription

Your customer pays $12,000 upfront for a 12-month subscription on January 1:

- Month 1 journal entry:

- Debit: Cash $12,000

- Credit: Deferred Revenue (liability) $12,000

- Each month (Jan–Dec):

- Debit: Deferred Revenue $1,000

- Credit: Revenue $1,000

After January's service delivery, you've earned $1,000 in revenue. The remaining $11,000 sits as deferred revenue, a liability on your balance sheet representing the service you still owe. That obligation carries real consequences if tracked poorly.

Why Deferred Revenue Matters

As your subscriber base grows, deferred revenue accumulates fast. Sloppy tracking creates problems across multiple fronts:

- Overstated earnings that misrepresent your actual financial position

- Misleading cash flow reports that mask how much service you still owe

- Audit and fundraising risk when your books don't align with recognized standards

According to FE International's M&A analysis, buyers scrutinize deferred revenue waterfalls during due diligence. It reveals renewal rates, fulfillment costs, and the overall quality of your revenue — details that directly affect your valuation.

Handling Mid-Contract Changes

Upgrades, downgrades, and cancellations mid-subscription complicate revenue recognition. Deloitte's ASC 606 guidance outlines how to account for contract modifications:

| Modification Type | Treatment | Example |

|---|---|---|

| Separate Contract | New, independent accounting | Customer adds distinct services at standalone prices |

| Prospective Reallocation | Terminate old, create new contract | Remaining services priced differently than standalone |

| Cumulative Catch-Up | Adjust existing contract | Remaining services not distinct from prior deliveries |

Each contract change requires an immediate adjustment in your accounting system. When you're managing a handful of customers, a spreadsheet can handle it. Once you're tracking dozens of modifications across different billing cycles, manual processes introduce errors that compound over time — exactly the kind of problem that shows up as a red flag during fundraising or acquisition due diligence.

Key SaaS Metrics Every Early-Stage Founder Must Track

MRR and ARR: Your North-Star Metrics

Monthly Recurring Revenue (MRR) is the predictable monthly subscription income from all active customers, accounting for new sales, upgrades, downgrades, and churn. Annual Recurring Revenue (ARR) is typically MRR × 12. According to OpenView's SaaS metrics guide, these are the first numbers investors scrutinize because they reveal the sustainability of your revenue engine.

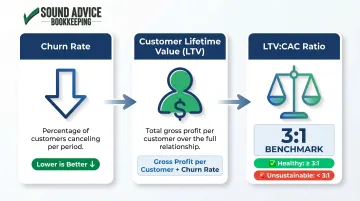

Churn and the LTV:CAC Ratio

Three metrics work together to reveal whether your growth model is actually profitable:

- Churn rate — the percentage of customers who cancel during a given period

- Customer Lifetime Value (LTV) — total gross profit generated by a customer over their entire relationship with you

- Customer Acquisition Cost (CAC) — the fully loaded cost to win one customer, including all sales and marketing expenses

Andreessen Horowitz emphasizes that LTV must use gross profit (not gross revenue), and CAC must include fully loaded costs. The 3:1 LTV:CAC ratio is the standard benchmark — a healthy SaaS business generates $3 in customer value for every $1 spent acquiring them. Ratios below 3:1 signal unsustainable growth economics.

The Rule of 40: Balancing Growth and Profitability

Popularized by venture capitalist Brad Feld in 2015, the Rule of 40 states that a healthy SaaS company's revenue growth rate (%) + profit margin (%) should equal or exceed 40%.

For example:

- A startup growing at 60% with a -20% EBITDA margin = 40% (meets threshold)

- A mature company growing at 15% with a 30% EBITDA margin = 45% (exceeds threshold)

Early-stage startups can use this benchmark to evaluate whether they're balancing growth investment with a path to profitability—especially when preparing for a funding round. However, Bessemer Venture Partners' 2025 "Rule of X" suggests weighting growth 2-3x more heavily than margin for late-stage cloud companies, because growth compounds while margin improvements are linear.

Common SaaS Accounting Mistakes Early-Stage Startups Make

Recognizing Revenue Too Early

The most damaging mistake: recording the full value of an annual contract as revenue in month one. This inflates short-term earnings, misleads investors, and creates sudden revenue "drop-offs" later that raise red flags during due diligence.

SEC enforcement actions against companies like Autonomy and Xerox show what's at stake: massive write-downs, regulatory investigations, and lasting reputational damage from premature revenue recognition.

Mixing Cash and Accrual Records

Founders using basic spreadsheets or mixing personal and business bank accounts often fail to track deferred revenue separately. Without clean separation between cash received and revenue earned, financial statements become unreliable — and that creates real problems:

- Reconciliation headaches at tax time

- Compliance exposure during audits

- Inaccurate revenue reporting that undermines investor confidence

Ignoring SaaS-Specific KPIs

Poor record-keeping often goes hand-in-hand with another gap: ignoring the metrics that actually measure subscription health. Operating entirely from a P&L statement without tracking MRR, churn, or LTV:CAC leaves you unable to answer basic investor questions and unable to spot early warning signs of retention problems. Traditional accounting metrics alone don't reveal whether your subscription engine is healthy or losing customers fast.

When to Bring in Professional SaaS Bookkeeping Help

Clear Trigger Points

Stop managing your own books when:

- Annual subscription contracts are in play and deferred revenue tracking becomes essential

- Multiple pricing tiers or add-ons complicate billing and revenue recognition

- An investor or bank requests audited or GAAP-compliant financial statements

- You're preparing for a funding round and need investor-ready financials quickly

Bookkeeper vs. Fractional CFO: Understanding the Difference

A bookkeeper maintains accurate day-to-day records, tracks deferred revenue, reconciles accounts, and produces monthly financial statements. A fractional CFO provides strategic forecasting, investor reporting, and fundraising guidance.

Early-stage startups typically need a specialized bookkeeper first. Firms like Sound Advice Bookkeeping function as an extension of your founding team, not just a vendor. Their model is built around three key advantages:

- QuickBooks expertise across Online, Desktop, and Enterprise platforms

- Flat-fee pricing starting at $170/month based on transaction volume, not time spent

- A three-phase onboarding process that configures your books correctly from day one

The ROI of Outsourcing Early

Outsourcing SaaS bookkeeping is more cost-effective than hiring a full-time accountant. Robert Half's 2026 salary data shows staff accountants command $73,750 annually (before benefits), while specialized bookkeeping services range from $2,268–$4,068 annually for early-stage startups.

That cost gap goes further than the salary comparison suggests. Outsourcing also helps you avoid compliance errors, get investor-ready financials faster, and focus on product and growth instead of QuickBooks reconciliation. When Matt Glick, CEO of Sage Catering, worked with Sound Advice Bookkeeping, he noted: "The bookkeepers are knowledgeable and work with us daily to keep things in order. If you are looking for competent bookkeepers to become an extension of your team, I highly recommend Sound Advice."

Frequently Asked Questions

What is SaaS bookkeeping?

SaaS bookkeeping is the ongoing process of recording and organizing a subscription-based company's financial transactions using accounting practices built for recurring revenue models. This includes tracking MRR/ARR, categorizing expenses, and managing deferred revenue — areas where standard bookkeeping methods fall short.

What is the best bookkeeping method for startups?

Accrual basis accounting is the recommended method for SaaS startups because it matches revenue to the period it's earned, not when cash is received. This produces accurate financial statements that reflect subscription performance and hold up to investor and regulatory scrutiny.

What is the Rule of 40 for SaaS companies?

The Rule of 40 is a SaaS benchmark where revenue growth rate (%) plus profit margin (%) should sum to 40% or higher. Investors use this metric to assess whether a startup balances growth investment with a credible path to profitability.

When should a SaaS startup switch from cash to accrual accounting?

Switch as soon as you begin taking subscription or multi-month prepayments—and certainly before seeking outside investment. Investors and lenders typically require GAAP-compliant (accrual) financial reporting, and transitioning during fundraising creates costly delays.

What is deferred revenue and why does it matter for SaaS startups?

Deferred revenue is the portion of a customer's upfront payment that hasn't been earned yet because the service hasn't been delivered. It sits on the balance sheet as a liability and is recognized gradually over the subscription term — a critical distinction for accurate SaaS financial reporting.

Do early-stage SaaS startups need to follow GAAP?

While GAAP compliance isn't legally required for private early-stage companies, following GAAP from the start builds investor trust, simplifies fundraising due diligence, and prevents the costly rework of financial records as your company scales.

Ready to get your SaaS accounting right from day one? Sound Advice Bookkeeping specializes in helping startups establish GAAP-compliant, investor-ready financial systems using QuickBooks. With bookkeeping services built for startups since 2009 and flat-fee pricing starting at $170/month, the team works as an extension of your founding team. Contact them at 303.228.8911 or schedule a consultation to discuss your specific needs.