Introduction

Construction businesses fail at alarming rates. Bureau of Labor Statistics data shows steep survival drop-offs in the construction sector, with establishments facing an 11.0% survival rate within their first year. Poor financial management drives much of this attrition. In 2024 alone, the construction industry lost $280 billion to slow payments, while subcontractor Days Sales Outstanding (DSO) climbed to 96 days—up from 90 in 2019. The numbers point to a clear pattern: cash flow problems kill construction businesses before bad projects do.

Construction bookkeeping is a survival skill, not a back-office function. This guide covers why it demands specialized expertise beyond standard accounting, the core practices that protect your profit margins, and how to choose between DIY, software, and professional help.

TLDR

- Job costing tracks every dollar to specific projects, revealing true profitability before it's too late to act

- Retainage withholds 5-10% of payments until completion, creating dangerous cash flow gaps that require separate tracking

- Construction payroll compliance is far more complex due to prevailing wages, multi-state rules, and subcontractor classifications

- Construction-specific software or professional services eliminate costly errors and turn raw financial data into actionable insight

- Clean books win better bids, secure financing, and support smarter growth decisions

Why Construction Bookkeeping Is Different from Standard Bookkeeping

Unlike retail or service businesses that track aggregate revenue and expenses, construction operates as a collection of independent financial entities. Each project has its own budget, timeline, crew, and cost structure. A contractor might simultaneously manage a profitable commercial build and a residential project bleeding money—but without project-level tracking, the overall ledger masks which jobs generate profit and which destroy it.

Construction adds layers of complexity that break standard bookkeeping methods. Multiple concurrent projects stretch across months or years, each exposed to unpredictable external forces: material price swings, weather delays, labor shortages, and subcontractor disputes. In 2025, 78% of construction firms struggled to fill hourly craft positions, while construction material prices rose 4.8% year-over-year.

Contract retainage, change orders, and milestone-based billing compound the challenge further. The financial mechanics of a construction firm have little in common with those of a coffee shop or consulting firm.

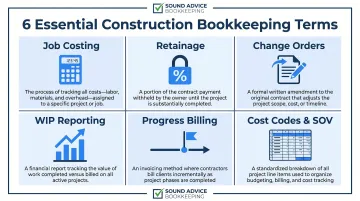

Essential construction bookkeeping terms you must know:

- Job costing: Tracks every expense against a specific project so you know exactly which jobs are profitable and which aren't

- Retainage: Typically 5–10% of each payment held back by the client until the project is fully complete

- WIP reporting (Work-in-Progress): Compares costs incurred to revenue recognized across all active jobs—essential for spotting budget drift early

- Change orders: Contract modifications that adjust scope and price, requiring immediate documentation to avoid disputes

- Progress billing: Invoices tied to completion milestones rather than a single end-of-project payment

- Cost codes and schedule of values: Paired tools that organize expenses by category (labor, materials, equipment) and break the contract price into phases, giving you line-item visibility throughout the build

Job Costing: The Cornerstone of Construction Bookkeeping

Job costing allocates every cost—direct and indirect—to specific projects. It's the most critical practice in construction bookkeeping because without it, you won't know whether a project is profitable until it's too late to act. Contractors who fully implement job costing systems see 10-20% profit margin increases within the first year by exposing underbidding, revealing costly job types, and improving labor efficiency.

Separating Direct and Indirect Costs

Direct costs tie directly to specific projects: labor wages for your crew, raw materials, equipment rentals, subcontractor fees. Indirect costs (overhead) support operations but don't belong to one project: insurance premiums, office utilities, administrative salaries, shop rent. Both must be assigned to individual projects to calculate true profitability.

Use cost codes to organize spending within each job:

- Labor: Track by crew, trade, or task phase

- Materials: Separate lumber, concrete, electrical, plumbing, etc.

- Equipment: Differentiate owned equipment costs from rentals

- Subcontractors: Track by trade and vendor

- Permits & fees: Capture regulatory costs

A construction-specific chart of accounts structures these categories logically, separating Cost of Revenues (direct costs) from Selling, General, and Administrative expenses (overhead). Best practices recommend using cost codes to categorize expenses rather than creating excessive subaccounts, keeping your chart of accounts clean while maintaining detailed job-level tracking.

Tracking Work-in-Progress (WIP)

That granular cost tracking feeds directly into WIP reporting, which provides a real-time snapshot of where each project stands financially and physically. It compares costs incurred against revenue recognized for incomplete projects, flags overbilling or underbilling situations, and gives you room to adjust before costs overrun projections.

Key WIP metrics to monitor:

- Costs in Excess of Billings (Underbillings): You've incurred costs but haven't billed clients yet — a cash flow warning sign

- Billings in Excess of Costs (Overbillings): You've billed more than you've spent, which creates short-term cash but risks drawing against funds you haven't yet earned

- Percentage of Completion: Work completed versus total contract value, which determines when revenue can be recognized

The Construction Financial Management Association (CFMA) considers an Underbillings-to-Equity ratio of 30% or less acceptable; the 2024 industry average was 8.1%.

Accurate job costing feeds these calculations, giving WIP reports real strategic value. They inform future bids, support bonding and financing applications, and reveal which project types generate the highest returns.

Managing Cash Flow, Retainage, and Revenue Recognition

Cash flow in construction operates differently from other industries. Payments arrive in waves tied to milestones. Expenses front-load before revenue arrives. Retainage locks up 5-10% of earned revenue until project completion. For an industry with notoriously thin margins, these dynamics create dangerous cash shortfalls. Nearly two-thirds of subcontractors cited cash-flow strain as their top business challenge entering 2025, with 53% reporting they dipped into retirement savings to float business expenses—a 147% increase from 2019.

Understanding and Tracking Retainage

Contract retainage typically withholds 5-10% of each progress payment until project completion. For contractors operating on 10-15% profit margins, retainage can consume half to all of your expected profit until final closeout. Record retainage separately as accounts receivable, not income. Counting it early overstates available cash and leads to spending money you haven't actually received.

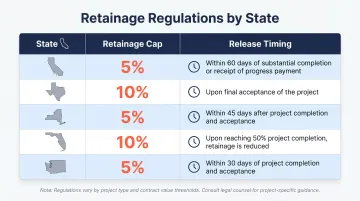

State retainage laws vary significantly:

| State | Retainage Cap | Release Timing |

|---|---|---|

| California | 5% (public works) | Within 60 days after completion |

| Texas | 5% (public ≥$5M); 10% (<$5M) | Upon work completion |

| New York | 5% (private works) | No later than 30 days after final approval |

| Florida | 5% (public ≥$200K) | Private works not regulated by statute |

| Washington | 5% (private & public) | Interest starts 30 days after acceptance |

Knowing your state's rules determines how aggressively you can plan around retainage release dates — and when to follow up if payment stalls.

Revenue Recognition Methods

Construction uses two primary revenue recognition methods, each with real consequences for financial reporting and tax obligations:

Percentage-of-Completion Method: Recognizes revenue as work progresses, based on costs incurred relative to total estimated costs. U.S. GAAP (ASC 606) requires this method when your performance creates or enhances assets the customer controls or you have enforceable right to payment for completed work. Best for long-term projects, it provides better cash flow visibility and matches revenue with actual progress.

Completed-Contract Method: Recognizes revenue only upon project completion. The IRS allows a "small contractor exception" under Section 460: contractors with average annual gross receipts under $31 million (for 2025) can use this method for projects completed within two years. It simplifies accounting but distorts profitability mid-project and creates uneven tax obligations.

Cash flow improvement strategies:

- Invoice at milestone stages — never wait until project completion to bill

- Send invoices immediately when a milestone is reached, not at the end of the week

- Negotiate 30-60 day payment terms with suppliers to extend your runway

- Maintain separate accounts for operating expenses, payroll, and incoming payments

- Run monthly cash flow projections so shortfalls show up on paper before they hit your bank account

Payroll, Compliance, and Record-Keeping Essentials

Construction payroll is uniquely complex and carries significant legal risk. Workers may earn prevailing wages set by state and local agencies, union rates, or different rates for different job classifications. Federal projects over $2,000 trigger Davis-Bacon Act prevailing wage requirements, mandating certified weekly payroll submissions preserved for three years.

Multi-state projects create additional payroll tax obligations in each jurisdiction. Subcontractors require proper 1099-NEC reporting for payments totaling $600 or more, and misclassifying employees as independent contractors triggers severe IRS and Department of Labor enforcement.

Record-keeping non-negotiables:

- Keep personal and business bank accounts completely separate — no exceptions

- Retain every invoice, receipt, contract, change order, and subcontractor agreement

- Reconcile bank statements against your books monthly to catch discrepancies early

- Follow the 3-2-1 backup rule: three copies of data, two storage formats, one stored offsite

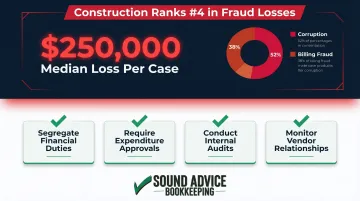

Good records alone won't protect you. The Association of Certified Fraud Examiners ranks construction fourth highest in median fraud losses, with a median loss of $250,000 per case — driven most often by corruption (52%) and billing fraud (38%). Internal controls are your primary defense:

- Segregate financial duties (different people for approvals, payments, and reconciliation)

- Require approval processes for expenditures above thresholds

- Conduct periodic internal audits

- Monitor vendor relationships for irregularities

Bookkeeping Software, Outsourcing, and When to Get Professional Help

Choosing the Right Construction Bookkeeping Software

General accounting software lacks the architecture construction demands. 75% of construction contractors use ERP systems, but choosing the wrong platform creates profit blind spots.

Construction-specific features to prioritize include:

- Job costing across multiple projects and cost codes

- WIP reporting and ASC 606 revenue recognition support

- Progress invoicing and AIA G702/G703 draw management

- Retainage tracking and certified payroll processing

- Subcontractor management and lien waiver tracking

- Real-time project-level financial dashboards

QuickBooks (with proper construction configurations or add-ons) serves many small to mid-sized contractors effectively when set up correctly. More specialized platforms like Foundation, Sage Intacct Construction, and CMiC offer deeper industry-specific functionality but come at higher price points.

Warning signs you've outgrown DIY bookkeeping:

- Managing more than two concurrent projects

- Can't determine which individual jobs are profitable

- Falling behind on invoicing or payroll

- Facing tax compliance concerns or audit notices

- Spending more time on books than on project management

At these points, the cost of errors exceeds the cost of professional help.

The Case for Outsourced Bookkeeping

Outsourcing construction bookkeeping delivers real advantages over keeping it in-house:

- Specialized expertise without the cost of a full-time hire

- Reduced risk of errors that damage bonding capacity or trigger audits

- More time focused on project management and business development

- Flexible support that scales with your project volume

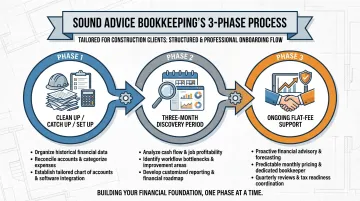

Sound Advice Bookkeeping brings 100+ years of combined QuickBooks expertise to construction and project-based businesses across 30+ states. Their 3-Phase Process is designed to understand your operation first, then build a bookkeeping structure that actually supports how you run jobs:

Phase 1 (Clean Up/Catch Up/Set Up): Organizes existing records or builds new systems from scratch — general ledger configuration, bank integrations, and a proper cost-tracking structure for labor, equipment, and subcontractors.

Phase 2 (3-Month Discovery Period): Maps your actual operations — project accounting requirements, seasonal cash flow patterns, payroll complexity, and vendor cycles — to calibrate your ongoing service.

Phase 3 (Ongoing Support - Flat Fee): Flat monthly pricing based on transaction volume (not hours worked), covering reconciliation, expense coding by project, payroll, AP/AR management, sales tax, and managerial reporting focused on growth and efficiency.

Having served over 1,000 small businesses, Sound Advice functions as an extension of your team—providing the financial clarity you need to win better bids, secure financing, and plan for sustainable growth.

Frequently Asked Questions

What is job costing in construction bookkeeping?

Job costing tracks all direct costs (labor, materials, equipment, subcontractors) and allocated indirect costs (overhead) to specific projects. This reveals true project-level profitability and informs future bidding strategies, so contractors price future work accurately and avoid underbidding.

What is retainage in construction bookkeeping?

Retainage is a portion of payment (typically 5-10%) withheld by clients until project completion as financial incentive for proper work. It must be tracked separately as accounts receivable, not income, to avoid misrepresenting available cash and making decisions based on money you haven't received.

What is the best bookkeeping method for a construction company?

Most construction companies use accrual-based, project-centric accounting with either the percentage-of-completion method or the completed-contract method. The right choice depends on project length, complexity, and whether you qualify for IRS small contractor exceptions.

How often should a construction company reconcile its accounts?

Reconcile monthly at minimum. For businesses handling high transaction volumes or multiple active projects, weekly reconciliation is advisable to catch discrepancies early and maintain accurate job costing data that informs real-time decisions.

What is the going hourly rate for a bookkeeper for a small construction business?

Bookkeeping and accounting clerks earn a mean hourly wage of $23.84, according to BLS data. Outsourced construction accounting services typically range from $1,500 to $6,500 per month depending on transaction volume and scope, often delivering better value than part-time hires through specialized construction expertise and fewer costly errors.

Is AI replacing bookkeepers for small construction businesses?

While 61% of construction firms report increasing AI investments in 2026, AI currently handles repetitive tasks like invoice processing and receipt capture. The judgment-heavy work — revenue recognition, job-cost allocations, retainage tracking — still requires experienced human oversight. AI assists; it doesn't replace.