Introduction

You started your nonprofit to change lives, not to wrestle with spreadsheets. Yet without clean, compliant books, the mission you're working so hard to advance is at risk. Nonprofit leaders face unique financial challenges that for-profit businesses never encounter: tracking donor restrictions, maintaining tax-exempt status, proving accountability to grantors, and preparing specialized financial statements that most business owners have never heard of.

Failing to file Form 990 for three consecutive years triggers automatic revocation of your 501(c)(3) status. Misusing restricted grant funds can force you to return thousands of dollars and damage relationships with funders.

According to the 2024 ACFE Report to the Nations, nonprofits represented 10% of occupational fraud cases, with a median loss of $76,000 — money that could have served your mission instead.

This guide covers everything nonprofit leaders need to navigate their finances with confidence:

- How nonprofit bookkeeping differs from for-profit accounting

- The four required financial statements

- Core bookkeeping duties and fund accounting essentials

- Compliance best practices to protect your tax-exempt status

- How to decide whether to handle bookkeeping in-house or outsource to specialists

Key Takeaways

- Nonprofit bookkeeping uses fund accounting to track restricted versus unrestricted funds, unlike for-profit equity accounting

- Four required financial statements: Statement of Financial Position, Statement of Activities, Statement of Functional Expenses, and Statement of Cash Flows

- Core duties include recording all transactions (including in-kind donations), monthly reconciliation, payroll, and fund cost allocation

- Accrual accounting is GAAP-compliant, audit-ready, and the preferred method for most nonprofits

- Outsourcing to nonprofit-specialized bookkeepers cuts compliance risk and frees staff for mission work

How Nonprofit Bookkeeping Differs from For-Profit

The foundational difference is structural: nonprofits have no owners and no equity accounts. Instead of tracking "retained earnings," you track net assets—resources available to advance your mission, categorized by donor restrictions. Revenue doesn't come primarily from sales; it comes from donations, grants, and program fees, each with unique recording requirements.

Bookkeeping vs. Accounting: Understanding the Distinction

Many nonprofit leaders use these terms interchangeably, but they represent distinct functions:

- Bookkeeping is the daily work of recording and organizing financial transactions—logging donations, paying vendors, reconciling bank accounts, processing payroll, and categorizing expenses

- Accounting involves analyzing that data, preparing financial reports, interpreting trends, advising leadership, and planning for the future

Both roles are essential. Bookkeepers produce the accurate data accountants need to generate meaningful insights. Small nonprofits often need both skill sets, though not necessarily two separate professionals.

Compliance Frameworks That Govern Nonprofit Books

Three frameworks shape how you must maintain and report your finances:

- GAAP (Generally Accepted Accounting Principles): The baseline standards that apply to all organizations, governing how transactions are recorded and reported

- FASB (Financial Accounting Standards Board): Sets nonprofit-specific reporting rules. FASB ASU 2016-14 overhauled nonprofit reporting in 2016, simplifying net asset classifications and requiring expenses to be reported by both function and nature

- Form 990: The IRS annual filing required to maintain 501(c)(3) tax-exempt status, due on the 15th day of the 5th month after your fiscal year ends—this public document pulls data directly from your financial statements

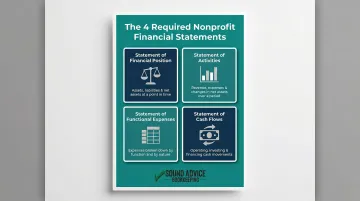

The Four Essential Financial Statements for Nonprofits

Statement of Financial Position

This is the nonprofit equivalent of a balance sheet. It shows your assets, liabilities, and net assets at a specific point in time—typically your fiscal year-end.

What appears under assets:

- Cash and cash equivalents

- Grants and pledges receivable

- Prepaid expenses

- Property, equipment, and vehicles

- Investments

What appears under liabilities:

- Accounts payable

- Accrued expenses

- Deferred revenue

- Long-term debt

Net assets classification: Under current FASB standards, you must separate net assets into two categories: net assets without donor restrictions (formerly unrestricted) and net assets with donor restrictions (combining what used to be temporary and permanently restricted). Endowments where only investment income can be spent fall under restricted net assets.

Statement of Activities

This document shows changes in your net assets over a period—typically a fiscal year. It's the nonprofit equivalent of an income statement, displaying revenue earned and expenses incurred.

FASB ASU 2016-14 requires you to separate restricted from unrestricted activity clearly. This statement answers the question: "Did we end the year with more or fewer resources than we started with, and why?" Board members and major donors rely on this document to understand your financial trajectory.

Statement of Functional Expenses

Nonprofit reporting becomes distinctive here. FASB now requires all nonprofits—not just health and welfare organizations—to report expenses in a matrix format showing:

- By function: Program services, management/general, fundraising

- By nature: Salaries, rent, supplies, professional fees, utilities, etc.

Why does this matter? Donors and grantors want proof you're spending money efficiently. This statement shows exactly how much of each dollar goes directly to programs versus overhead. A nonprofit spending 85% on programs and 15% on administration tells a different story than one spending 50% on fundraising.

Statement of Cash Flows

This tracks actual cash movement through three categories:

- Operating activities: Day-to-day cash from donations, grants, program fees, and vendor payments

- Investing activities: Buying or selling property, equipment, or investments

- Financing activities: Borrowing money or repaying loans

Your Statement of Activities uses accrual accounting—recording revenue when earned and expenses when incurred—which can show a healthy surplus even when your bank account is low. The Statement of Cash Flows cuts through that, revealing actual liquidity: the cash available to pay bills this month.

Form 990: Your Annual Public Filing

Every 501(c)(3) organization must file Form 990 annually to maintain tax-exempt status. According to the IRS auto-revocation rules, organizations that fail to file for three consecutive years automatically lose their exemption.

Form 990 is public record—anyone can request it, and platforms like GuideStar publish it online. Well-maintained books throughout the year make this filing straightforward. Scrambling to reconstruct a year's worth of transactions in April leads to errors that can trigger IRS scrutiny. The Statement of Functional Expenses feeds directly into Form 990, Part IX—another reason consistent monthly bookkeeping pays off at filing time.

Core Bookkeeping Duties for Nonprofits

Recording Every Transaction with Audit-Ready Detail

Every financial event must be recorded with enough detail to support audits, grant reports, and donor inquiries:

- Cash donations: Date, donor name, amount, restricted or unrestricted

- In-kind donations: Fair market value, description, donor, date received—for example, a donated vehicle requires make, model, year, and FMV per IRS Publication 526

- Pledges: ASC 958 requires recognizing unconditional promises to give as receivables when received

- Grant receipts: Tracking restrictions, reporting deadlines, and allowable expenses

- Vendor payments: Invoice details, check number, payment date, expense category

Bank Reconciliation: Your First Line of Defense

Compare your internal records to bank statements at minimum monthly—weekly for high-volume organizations. For nonprofits, this matters because:

- It catches unauthorized transactions before they snowball

- It corrects recording errors before year-end close

- It deters internal fraud (knowing someone is watching)

According to the 2024 ACFE Report, the median fraud loss for nonprofits was $76,000. Regular reconciliation is one of the simplest fraud prevention tools available.

Processing Payroll and Managing Invoices

Payroll is a core bookkeeping responsibility in small-to-midsize nonprofits. Critical tasks include:

- Tracking employee classifications (employees receive W-2s; contractors receive 1099s)

- Withholding and remitting payroll taxes correctly

- Recording employer tax obligations

- Managing benefits deductions

Invoice management runs in both directions:

- Accounts receivable: Send invoices for fee-for-service programs and track incoming payments

- Accounts payable: Receive vendor invoices, obtain approvals, pay on time, and record each expense

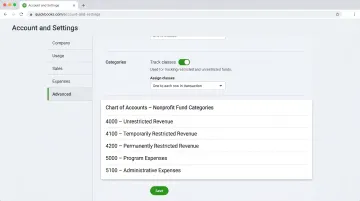

Allocating Costs to the Correct Funds

This is where nonprofit bookkeeping diverges sharply from for-profit work. When a foundation gives you $25,000 restricted to youth programming, you cannot use that money for rent, marketing, or general operations—even if you desperately need it.

Your Chart of Accounts is what makes compliance possible. Tailor it to your program areas, with separate codes or "classes" for each fund. For example:

- Unrestricted General Operating Fund

- Youth Services Program (ABC Foundation Grant)

- Capital Campaign Fund

- Endowment Fund

Every expense must be charged to the appropriate fund. Misallocating a restricted expense can trigger grant clawbacks, IRS scrutiny, or funder audits.

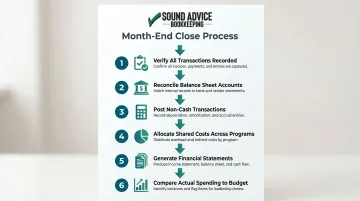

Month-End and Year-End Close

Closing the books each period involves:

- Verifying all transactions are recorded

- Reconciling all balance sheet accounts

- Posting non-cash transactions (depreciation, prepaid adjustments)

- Allocating shared costs across programs

- Generating financial statements

- Comparing actual spending to budget

Consistent monthly close procedures prevent year-end chaos. When December arrives, you're simply closing one more month—not reconstructing twelve months of financial activity under deadline pressure.

Fund Accounting: Managing Restricted vs. Unrestricted Funds

Nonprofit bookkeeping doesn't work like a standard business ledger. Because donors and grantors often restrict how their money can be used, you must track multiple "buckets" simultaneously—not just a single bottom line.

Two Primary Fund Categories Under Current Standards

FASB ASU 2016-14 simplified net asset classifications to two categories:

| Net Asset Type | What It Means | Examples |

|---|---|---|

| Without Donor Restrictions | Use for any legitimate organizational purpose | General operating donations, unrestricted grants, earned revenue |

| With Donor Restrictions | Subject to donor-imposed conditions | Grants restricted to a specific program, donations earmarked for equipment, endowment principal |

Common restricted fund examples include:

- A $50,000 grant restricted to a specific literacy program

- A $10,000 donation restricted for new computers

- An endowment where only investment earnings can be spent (principal is off-limits)

The Compliance Risk of Commingling Funds

What happens when you accidentally (or intentionally) spend restricted grant money on unallowed expenses? Under the OMB Uniform Guidance, federal awarding agencies can:

- Temporarily withhold payments

- Disallow costs and demand repayment

- Suspend or terminate the award entirely

- Initiate suspension or debarment proceedings

The consequences extend beyond federal grants. Private foundations can demand returned funds, exclude you from future grants, and share noncompliance information with other funders—causing lasting damage to your reputation in the nonprofit community. Treating restricted funds as a fiduciary obligation, not an accounting formality, is what protects your organization from these outcomes.

How Bookkeepers Track Restricted Funds in Practice

Your bookkeeper implements fund accounting through:

- Tagging every transaction by fund, program, or grant in QuickBooks (not just by expense type like salaries or rent)

- Recording restriction releases when conditions are met—for example, purchasing the donor-specified computers triggers a reclassification entry from restricted to unrestricted, documenting that you've fulfilled the obligation

- Tying the bookkeeping system directly to grant reporting deadlines so a foundation's spending report takes minutes to generate, not days

Nonprofit Bookkeeping Best Practices

Implement Internal Controls

Segregation of duties is your first defense against both accidental errors and intentional fraud. The person who authorizes transactions should not be the same person recording them or reconciling accounts. The National Council of Nonprofits recommends basic policies such as ensuring the person who logs checks isn't the person depositing them.

Small nonprofits struggle with this—when you only have three staff members, perfect segregation is impossible. In these cases, compensating controls become critical:

- Require dual signatures on checks over a threshold ($1,000, for example)

- Have board members review financial statements monthly

- Conduct periodic surprise audits

- Require annual independent audits (many states mandate this above certain revenue levels)

The 2024 ACFE Report found that 10% of occupational fraud cases occurred in nonprofits, with a median loss of $76,000. Strong internal controls sharply reduce this risk.

Use Accrual Accounting and the Right Software

Cash basis accounting is simpler—you record income when cash arrives and expenses when you pay bills. But accrual accounting gives a more accurate picture of financial health by recording income when earned and expenses when incurred, regardless of cash timing.

Accrual accounting is required for GAAP compliance—essential for audits and larger grant applications. A $100,000 grant awarded in December but not received until January appears on your December statements, matching revenue to the year it was earned.

The right software matters. QuickBooks, when configured for nonprofits, automates fund tracking and generates required reports with far less manual effort. Key nonprofit-specific configurations include:

- Chart of accounts templates built for fund accounting

- Fund and class tracking to separate restricted and unrestricted revenue

- Restricted revenue management to flag grant spending rules

Maintain Realistic Budgets and Reconcile Regularly

Budget-to-actual comparison should be a monthly discipline. Nonprofits that track budget versus actual spending throughout the year avoid painful surprises in November when they discover they've overspent program budgets or fallen short on fundraising projections.

Historical data is just as valuable. Keeping past budgets alongside actual expenditures improves future forecasts—if your annual gala consistently brings in 20% less than projected, that pattern should drive your planning, not wishful thinking. Over time, this discipline turns your budget from a guessing exercise into a reliable financial roadmap.

DIY vs. Outsourcing: Staffing Your Nonprofit's Books

When In-House Bookkeeping Works (and When It Doesn't)

Small nonprofits with minimal transactions—perhaps a dozen donations monthly, one or two grants, few vendors—can often manage with a financially savvy staff member or volunteer. This approach breaks down as complexity grows:

- Transaction volume exceeds 50-100 monthly

- Multiple restricted grants require separate tracking

- Grant reporting deadlines pile up

- State audit thresholds approach (varies by state: $500,000 in Illinois, $1,000,000 in Florida, $2,000,000 in California)

- Federal single audit threshold of $1,000,000 is reached

Qualifications to seek in an in-house bookkeeper:

- Experience with nonprofit accounting software

- Understanding of fund accounting principles

- Familiarity with Form 990 requirements

- Knowledge of state charitable solicitation regulations

- Comfort with GAAP and accrual accounting

The Case for Outsourcing to Nonprofit-Specialized Bookkeepers

Outsourcing provides access to experts who already understand fund accounting, Form 990 requirements, and GAAP compliance—without the cost of a full-time salary plus benefits.

Sound Advice Bookkeeping, for example, works as an extension of your team rather than just a vendor. Managing Partner Dr. Ali Hill brings over two decades of running nonprofit organizations, an MPA from Columbia University's School of International and Public Affairs, and a PhD in Sociology — credentials that translate directly into practical financial guidance for mission-driven organizations.

A strong outsourced partner does more than record transactions. They configure QuickBooks for nonprofit-specific needs, establish proper fund tracking, and deliver financial statements ready for board review or grant reporting.

Starting at $170 per month based on transaction volume, outsourced bookkeeping often costs less than hiring even a part-time employee — with access to expertise a generalist hire rarely matches.

Key Questions to Ask When Evaluating Bookkeeping Support

The right questions reveal whether a bookkeeper truly understands the nonprofit sector — or just knows how to process transactions. Whether hiring in-house or outsourcing, ask:

- Confirm nonprofit-specific experience — generic small business bookkeeping doesn't translate directly to 501(c)(3) compliance

- Ask how they coordinate with your CPA and auditor; seamless collaboration is non-negotiable at tax time

- Clarify the month-end close process — financial statements should arrive within 10-15 days after month-end

- Request specifics on restricted fund handling; vague answers here are a red flag

- Understand the pricing structure — flat-fee monthly pricing helps nonprofits budget accurately, while hourly billing can fluctuate unpredictably

Frequently Asked Questions

Do nonprofits need bookkeeping?

Yes, bookkeeping is both a legal obligation and a practical necessity. It's required for Form 990 filing and maintaining tax-exempt status, and it's essential for managing donor funds responsibly and meeting grantor reporting requirements.

What does a bookkeeper do for a nonprofit?

A nonprofit bookkeeper handles the core financial work that keeps your organization compliant and operational:

- Records all financial transactions and reconciles bank accounts monthly

- Manages payroll, invoices, and cost allocation across restricted and unrestricted funds

- Produces financial statements used by leadership and accountants for decisions and compliance

What is the most desirable method of accounting for a nonprofit?

Accrual accounting is the preferred and GAAP-compliant method. It records income when earned and expenses when incurred—regardless of cash timing—giving a more accurate picture of financial health than cash basis accounting. It's required for audits and most grants.

What are the four basic financial statements for a nonprofit?

The four required statements are the Statement of Financial Position, Statement of Activities, Statement of Functional Expenses, and Statement of Cash Flows. Form 990, the annual IRS filing, is also required and draws data from these statements.

How long does a 501(c)(3) need to keep records?

IRS Publication 4221-PC sets the following minimum retention guidelines:

- Financial records: at least 7 years

- Employment tax records: at least 4 years after filing the fourth quarter return

- Permanent records (articles of incorporation, bylaws, determination letter): indefinitely

What is the 33% rule for nonprofits?

The public support test requires that at least one-third (33%) of a 501(c)(3)'s total support come from public sources—such as individual donors and government grants—rather than a small number of large donors or investment income. This is measured over a five-year computation period. Accurate bookkeeping is essential for tracking and documenting these revenue sources.