Introduction

Most small business owners started their companies to pursue a passion — serving customers, building something meaningful, or solving a problem no one else was solving. No one launched a business to spend evenings reconciling bank statements, chasing down receipts, or panicking when tax season rolls around.

Yet as operations grow, bookkeeping becomes one of the biggest time drains and sources of financial risk. Without organized records, owners miss tax deductions, misread profitability, and end up making decisions based on a checking account balance rather than real financial data.

The typical response creates its own problem: handle it yourself at the cost of your time and accuracy, or delay it until the backlog turns into a crisis.

Outsourced bookkeeping offers a practical middle ground. This guide covers what it actually involves, what it costs, and how to know if it's the right move for your business — so you can make that decision with clear information rather than guesswork.

Key Takeaways

- Outsourced bookkeeping means hiring a third-party professional to manage your financial records, reconciliations, and reporting remotely

- Small businesses save 40-60% on accounting costs compared to hiring full-time staff

- Frees up an average of 20 hours per week owners currently spend on financial admin tasks

- Bookkeeping mistakes cost small businesses an average of $3,534 in overpaid taxes annually — professional accuracy prevents that

- Monthly financial reviews give owners clear visibility into cash flow, expenses, and tax readiness year-round

What Is Outsourced Bookkeeping (and How Does It Work)?

Outsourced bookkeeping means hiring an external professional or firm to handle the day-to-day financial record-keeping that keeps a business financially healthy. Rather than managing books yourself or hiring a full-time employee, you partner with specialists who maintain accurate records, prepare reports, and keep you compliant with tax requirements.

Core tasks typically covered include:

- Recording income and expense transactions

- Bank and credit card reconciliation

- Accounts payable (vendor payments) and receivable (customer collections)

- Payroll support and processing

- Financial statement preparation (balance sheets, income statements, cash flow reports)

- Sales tax payment management

- Tax preparation support

How it works in practice:

The business grants the bookkeeper secure access to financial accounts and accounting software like QuickBooks. The bookkeeper manages transactions, categorization, and reconciliations behind the scenes — usually on a monthly cycle. You receive organized, up-to-date financial reports that show exactly where your business stands without handling the tedious details yourself.

In practice, it works like having a part-time finance department — you stay informed through monthly reports and regular check-ins, without touching a single spreadsheet yourself.

Key Benefits of Outsourcing Bookkeeping for Small Businesses

Outsourcing bookkeeping delivers measurable changes to cost, time, and accuracy — here's what that looks like in practice.

Significant Cost Savings Compared to In-House Hiring

Outsourcing eliminates the fixed costs of a full-time employee — salary, benefits, payroll taxes, training, and turnover expenses — replacing them with a flexible, predictable monthly fee scaled to your actual needs.

The numbers tell the story:

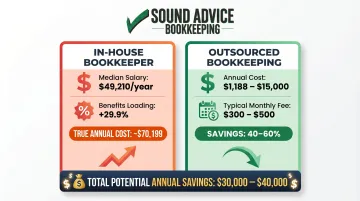

The median salary for a U.S. bookkeeper is $49,210 annually, but employer-loaded benefits add 29.9% to total compensation, bringing the true cost to approximately $70,199 per year. Outsourced bookkeeping services typically cost $1,188 to $15,000 annually depending on transaction volume — representing 40-60% savings on finance operations.

Hidden costs you avoid:

- Software subscriptions and accounting tools

- Continuing education and professional certifications

- Sick days, vacation time, and paid leave

- Recruitment and training expenses when employees leave

- Office space and equipment

Predictable flat-fee pricing lets you budget accurately without surprise payroll expenses during slow seasons. For a business with 100-200 monthly transactions, professional outsourced bookkeeping often costs $300-500 per month — a fraction of what you'd pay for even a part-time in-house bookkeeper.

This matters most for early-stage businesses where every dollar counts, and for operations with fluctuating workloads that don't justify year-round staffing.

Time Back to Focus on What Actually Grows Your Business

Bookkeeping is detail-intensive and time-consuming. When owners handle it themselves, they trade high-value strategic time for administrative work that trained professionals complete more efficiently.

Small business owners spend an average of 20 hours per week on accounting and financial tasks. At $150 per hour of owner time, this represents a $36,000 annual opportunity cost — time that could be spent on sales, client work, product development, or strategic planning.

Beyond just hours saved:

Outsourcing removes the cognitive load of monitoring finances, hunting down receipts, and worrying about accuracy. That recovered mental bandwidth is what lets owners shift from scrambling to planning — catching opportunities instead of chasing problems.

Professional bookkeepers also catch issues busy owners typically miss: overdue receivables aging beyond 60 days, unnecessary recurring expenses that could be cancelled, and uncategorized transactions that create tax reporting problems.

For businesses preparing to hire, expand, or seek financing — where clean financial documentation is non-negotiable — reclaiming this time is especially critical.

Accuracy, Expertise, and Built-In Fraud Prevention

Outsourced bookkeepers bring specialized training, industry knowledge, and systematic processes that reduce errors and catch irregularities untrained eyes miss.

Why professional accuracy matters:

Bookkeeping mistakes compound over time. A miscategorized expense today becomes a tax filing problem in April. Accounting errors result in an average of $3,534 per year in tax overpayments for small businesses. Professional bookkeepers use structured reconciliation processes that catch discrepancies before they escalate.

Fraud protection through separation of duties:

Organizations with fewer than 100 employees suffer a median fraud loss of $141,000, with 32% of cases driven by lack of internal controls. Outsourcing naturally introduces separation of duties — the person recording transactions is not the person authorizing payments. This structural control is one of the most effective defenses against internal fraud and accounting manipulation.

Staying compliant:

Professional bookkeepers stay current on tax law changes, deduction rules, and reporting requirements. They know which expenses qualify for deductions, how to properly categorize transactions for tax purposes, and what documentation the IRS requires. This reduces penalty risk while maximizing legitimate tax savings.

If untrained staff currently handle your books — or rapid growth has added transaction complexity — professional oversight becomes less of a convenience and more of a financial safeguard.

Signs It's Time to Outsource Your Bookkeeping

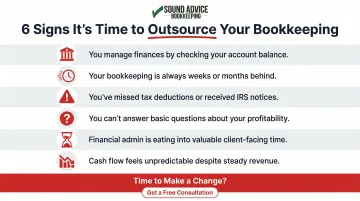

Most small business owners wait too long — outsourcing reactively after a tax problem or cash flow crisis rather than getting ahead of one. If any of these patterns sound familiar, it's time to bring in professional help:

You're running your business from your checking account balance rather than organized financial reports. Cash flow decisions made on instinct — not data — mean you can't confidently answer whether you can afford that equipment purchase or new hire.

Bookkeeping tasks are perpetually behind. Receipts pile up, accounts go unreconciled for months, and tax season becomes a panicked scramble to rebuild records from bank statements.

You've missed tax deductions or received IRS notices. Inaccurate categorization, late filings, and estimated payment errors cost real money — and the compliance headaches they create tend to compound.

Your books can't answer basic profitability questions: true margins, which expense categories drain the most cash, or which revenue streams actually generate profit after costs. That's not a gap you can manage around indefinitely.

Financial admin is eating into client time. If bookkeeping consumes more than a few hours a month, the ROI on your time is negative. According to HBK CPAs & Consultants, 67% of entrepreneurs say administrative burdens prevent them from focusing on growth.

Cash flow feels unpredictable despite consistent revenue. The Federal Reserve's 2025 Report on Employer Firms found that 51% of small employer firms cite uneven cash flow as a primary financial challenge. Without accurate books, the patterns behind your cash crunches stay invisible — and seasonal fluctuations catch you off guard every time.

How to Get the Most From Your Outsourced Bookkeeping Partner

Outsourced bookkeeping delivers maximum value when treated as an ongoing partnership, not a hands-off service you forget about until tax season. The relationship works best when expectations are clear from the start.

What a successful engagement looks like:

- Monthly financial reviews that keep you informed on cash flow trends, expense patterns, and what's changing

- Reliable communication channels for questions, document sharing, and transaction clarification — so nothing falls through the cracks

- Proactive observations beyond clean numbers: expense trends, receivables aging, and opportunities to improve your financial operations

The best providers function as an extension of your business rather than just a vendor. They understand your goals, your industry, and your growth plans — so their reports come with context, not just figures.

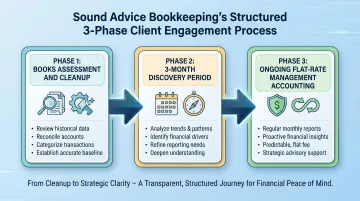

Sound Advice Bookkeeping, for example, uses a structured 3-Phase process. Phase 1 assesses and cleans up your current books. Phase 2 runs a 3-month discovery period to understand your specific transaction patterns. Phase 3 delivers ongoing management accounting at a predictable flat monthly rate. Clients know exactly what to expect — and make decisions based on real numbers.

To maximize your partnership:

- Keep your bookkeeper informed about upcoming large purchases or business changes

- Respond promptly to requests for receipts or transaction clarification

- Review monthly reports and ask questions when something looks unexpected

- Use the insights to drive strategic decisions — not just check a compliance box

Conclusion

Outsourced bookkeeping gives you something an in-house spreadsheet rarely can: a clean, consistent financial foundation that every business decision can actually rely on. A good bookkeeping partner transforms it from a dreaded obligation into a strategic asset — one that supports growth rather than just documenting it.

Those benefits build on each other over time:

- Accurate books mean better tax outcomes and fewer year-end surprises

- Clean financial statements make it easier to secure financing when you're ready to expand

- Reclaimed owner time goes back into selling, serving clients, and building the business

The earlier a small business outsources, the sooner it stops reacting to financial crises and starts planning with confidence. You didn't start your business to reconcile bank statements. Professional bookkeeping support puts that work in the hands of people who do it every day, so you can get back to the work only you can do.

Frequently Asked Questions

How does outsourced bookkeeping work?

You grant a third-party bookkeeper secure access to your financial accounts and accounting software. They handle transactions, reconciliations, and reporting in the background, then deliver organized financial reports — typically monthly — so you stay informed without managing the day-to-day details.

Why should you outsource your bookkeeping?

Outsourcing reduces costs 40-60% compared to in-house hiring, frees up 20+ hours weekly that owners currently spend on financial admin, and brings professional accuracy that prevents tax mistakes costing an average of $3,534 annually. You gain expertise and time without the overhead of a full-time employee.

How much can a small business save by outsourcing bookkeeping?

A full-time bookkeeper costs approximately $70,199 annually including benefits, while outsourced services typically range from $1,188 to $15,000 per year depending on transaction volume. Most small businesses with moderate transaction volumes save $30,000–$40,000 annually by outsourcing instead of hiring in-house.

What is the going hourly rate for a bookkeeper?

Freelance bookkeepers charge $11–25 per hour depending on experience and complexity, with a median around $20.85. Many small businesses prefer flat monthly fees ($300–500 for typical volumes) for predictability, since hourly costs can swing unpredictably as transaction volume changes.

When should a small business start outsourcing bookkeeping?

The best time is earlier than most owners expect, ideally before problems like missed deductions, inaccurate cash flow tracking, or tax-season panic arise. Even pre-revenue businesses benefit from clean books from the start, since fixing bookkeeping mistakes later costs far more than preventing them upfront.

Is my financial data safe with an outsourced bookkeeper?

Reputable providers use encrypted, cloud-based systems with role-based access controls. Keep sole authority over treasury functions — signing checks and authorizing payments — while granting the bookkeeper read and categorization access only. That separation of duties protects against fraud while keeping your records accurate.