Introduction

Higher education finance teams juggle hundreds of vendors across decentralized departments, strict grant compliance requirements, faculty reimbursements, student stipends, and end-of-fiscal-year crunches—typically with lean staff and aging systems.

Most corporate AP departments don't face this combination at once. In higher education, it's the daily baseline.

Higher education turnover remains elevated at 13.4%, while the pool of full-time, non-exempt staff who traditionally handle transactional processing has shrunk by 9% since 2017. This talent crunch hits AP operations particularly hard, leading to invoice backlogs, weakened internal controls, and heightened compliance risks under federal Uniform Guidance and IRS regulations.

This guide examines the unique AP landscape in higher education, common pain points facing finance teams, what effective AP services look like, and how institutions can choose between in-house, outsourced, or automated approaches based on their specific circumstances.

Key Takeaways

- Higher education AP spans multiple funding streams—each with distinct documentation and compliance requirements

- Compliance with 2 CFR Part 200 (Uniform Guidance) and IRS rules is non-negotiable—NSF audits have produced hundreds of thousands in disallowed costs

- Key pain points: ERP transitions, decentralized purchasing, invoice backlogs, and chronic staffing shortages

- AP can be managed in-house with automation, outsourced to a specialist, or handled through a hybrid model

- Smaller colleges often benefit from boutique partners who function as an extended finance team

What Makes Accounts Payable in Higher Education Uniquely Complex

Multi-Stream Funding Architecture

Higher education AP operates across multiple concurrent funding sources — a complexity most corporate environments never face. U.S. degree-granting institutions manage total revenues reaching $993 billion annually, including tuition revenue, state appropriations ($129.8 billion in fiscal year 2023), federal grants, endowment funds, and auxiliary enterprises like dining and bookstores.

Each funding stream carries its own payment rules, documentation standards, and compliance requirements. Mixing them up results in audit findings and disallowed costs.

Decentralized Purchasing Across Dozens of Departments

Unlike centralized corporate AP departments, universities have decentralized buying across facilities, research labs, athletics, dining services, academic departments, and administrative units. Each generates invoices that must be tracked, approved, and coded to the correct fund. This decentralization creates multiple submission channels, inconsistent approval workflows, and limited visibility for central finance teams trying to manage cash flow or prepare for board meetings.

Grant Fund Compliance Requirements

Federal and state grant purchases — from NSF and NIH to Department of Education and state workforce funds — must comply with specific procurement rules, allowability standards under 2 CFR Part 200, and strict documentation protocols. NSF Office of Inspector General audits have questioned or disallowed hundreds of thousands of dollars at major universities for:

- Inadequately supported expenses

- Inappropriately allocated expenses

- Professional service agreements executed after work began

- Indirect costs improperly applied

One audit of Yale University questioned $251,973 and disallowed $172,213 for unallowable and improperly allocated expenses. Grant-funded AP errors aren't just procedural — they carry real financial consequences.

Volume and Variety of Payables

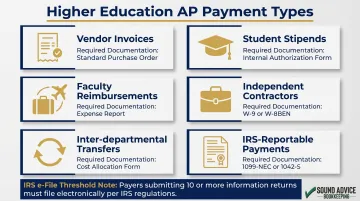

Higher education AP includes a wider variety of payment types than most corporate environments:

- Vendor invoices for goods and services

- Student stipends and graduate assistant payments

- Faculty expense reimbursements and travel advances

- Independent contractor payments (visiting lecturers, consultants)

- Inter-departmental transfers and cost allocations

- IRS-reportable payments requiring 1099-NEC or 1099-MISC filing

Each payment type requires different approval workflows, tax documentation, and withholding calculations. Domestic contractors need a Form W-9; nonresident aliens require Form W-8BEN or Form 8233. The IRS e-file threshold also dropped to 10 aggregate information returns for filings on or after January 1, 2024 — pushing even smaller institutions into electronic filing systems.

ERP Complexity and System Migrations

Many institutions are mid-transition between legacy systems (Banner, Oracle) and modern cloud platforms (Workday, Ellucian). These transitions create temporary control gaps and data integrity risks.

One large research university transitioning to Workday Financials experienced system integration issues that caused a massive AP backlog, requiring emergency external staffing to manually enter and validate financial records. A dedicated team of six AP professionals completed the cleanup in four months — two months ahead of the original projection — but only after the institution acknowledged the crisis and brought in outside help.

Common AP Challenges Facing Higher Education Finance Teams

Invoice Backlog and Processing Delays

High transaction volume combined with manual approval chains leads to invoice queues that stretch payment timelines from days to weeks or months. These backlogs strain vendor relationships, result in late fees, and create year-end audit headaches when finance teams scramble to reconcile months of pending invoices.

At institutions with chronic understaffing, the problem compounds: the more invoices pile up, the less time staff have to process them, and backlogs grow faster than teams can clear them.

Compliance and Audit Risk

Incomplete documentation, miscoded fund allocations, and missed three-way matching (purchase order, receiving report, invoice) create exposure during state audits, federal single audits under Uniform Guidance, or Board of Trustees financial reviews. North Dakota state audits revealed hundreds of thousands of dollars in unreconciled accounting errors across multiple state colleges, which campus officials attributed to severe understaffing and high turnover.

One university cycled through four financial controllers in six years — a turnover rate that directly erodes the institutional knowledge needed to maintain reliable financial controls.

A 2026 operational audit of the University of Florida found $2.4 million in unapproved P-card and virtual air card charges languishing as prepaid expenses due to processing delays and ineffective monitoring controls. When AP breaks down, the damage doesn't stay in accounts payable — it surfaces in audit findings, compliance violations, and reputational risk across the institution.

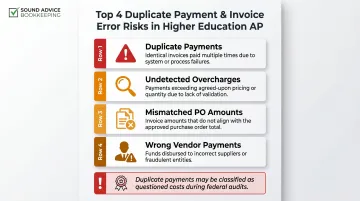

Duplicate Payments and Invoice Errors

Decentralized departments submitting invoices through multiple channels (email, mail, vendor portals, direct to department) increases the risk of:

- Duplicate payments when the same invoice enters the system twice

- Overcharges that go undetected without proper three-way matching

- Mismatched amounts between purchase orders and invoices

- Payments to incorrect vendors due to similar names

Recovering overpayments requires vendor cooperation and takes time most AP teams don't have. In grant-funded environments, the stakes are higher — duplicate payments can be classified as questioned costs during audits, triggering compliance reviews that strain already stretched staff.

Staffing Gaps and Turnover

Higher education finance offices frequently struggle with hiring and retaining experienced AP staff. The pool of full-time, non-exempt staff has decreased by 9% since 2017, creating sustained pressure on AP departments. During vacancies, remaining team members absorb additional workload in ways that increase error rates and processing times. Institutional knowledge walks out the door with departing staff, leaving new hires to navigate complex fund structures and departmental relationships without adequate training or documentation.

Poor Visibility and Reporting

Without centralized tracking and real-time reporting, finance leaders have limited visibility into what is owed, what is overdue, and how spending aligns to budget. Manual systems or poorly configured ERP modules make it difficult to produce aging reports by fund or department, leaving leadership unable to answer basic questions at board meetings: How much do we owe? When are payments due? Are we on track with budget? Without that data, finance directors are reacting to problems rather than preventing them — and cash flow management becomes guesswork.

Key Components of Effective AP Services for Higher Education

Invoice Receipt and Processing

Well-managed AP services handle the front end systematically — receiving invoices from multiple channels, digitizing paper documents, validating against supporting documentation, and routing for appropriate approval based on fund source and dollar amount.

Intake channels typically include:

- Email and vendor portals

- Mail and departmental submissions

- Purchase order and receiving report matching

This systematic intake prevents invoices from getting lost, ensures consistent handling regardless of source, and creates an auditable paper trail from receipt to payment.

Fund Coding and Compliance Documentation

For higher education specifically, AP services must include accurate fund allocation coding to ensure expenses are charged to the correct budget line, grant, or cost center. Compliance drives this requirement. Under 2 CFR Part 200, institutions must maintain documented procurement procedures and internal controls.

The micro-purchase threshold increases from $10,000 to $15,000 effective October 1, 2025, but institutions may self-certify thresholds up to $50,000 if they qualify as low-risk auditees.

Effective AP services ensure that fund coding is supported by documentation sufficient for audit purposes—including:

- Proper allocation formulas for shared expenses

- Grant budget category alignment

- Allowability determinations for questioned items

- Supporting documentation retained according to federal requirements (generally 3 years from final expenditure report)

Vendor Payment Management and Relationship Support

Timely payment processing across ACH, check, and wire maintains vendor trust and captures early payment discounts where available. AP teams handle vendor communication on payment status, resolve inquiries without burdening department heads, and sustain relationships that matter during contract negotiations or urgent purchases.

Payment timing is particularly critical in higher education, where smaller vendors (local bookstores, independent contractors, community organizations) may have limited cash reserves and depend on timely payment to meet their own obligations.

Reporting, Reconciliation, and Audit Readiness

Solid AP operations produce regular aging reports by fund and department, payment summaries that tie to the general ledger, and reconciliation statements supporting year-end preparation. Finance leadership gets a clean, auditable record at any point in the fiscal year — essential during state audits, federal single audits, or board financial reviews.

Top-performing AP operations achieve invoice processing cycle times of just 3.1 days compared to 17.4 days for lagging organizations — a gap that reflects the measurable impact of systematic processes and the right tools.

Best Practices for Managing AP in Higher Education Institutions

Standardize the purchase-to-pay workflow: Document and enforce an institution-wide process covering requisitions, purchase order issuance, goods receipt, invoice approval, and payment. When every department follows the same sequence, you reduce errors and create a clear audit trail.

Standardization doesn't eliminate departmental autonomy. It ensures that regardless of who's buying, the controls and documentation stay consistent.

Implement three-way matching as a control: Matching the purchase order, receiving report, and vendor invoice before releasing payment prevents overpayments, duplicate payments, and unauthorized purchases. University policy requires this match to be completed before payment is released.

This control is especially critical for grant-funded expenditures, where questioned costs can result in disallowed expenses and lost funding. Modern ERP systems enforce three-way matching automatically, sharply reducing the risk of payment errors without relying on manual review.

Establish regular AP review cycles and reporting: Finance teams should run monthly AP aging reviews and produce departmental spending summaries that department heads can validate before fiscal year close.

Regular review cycles catch problems early, including:

- Duplicate invoices submitted across billing periods

- Miscoded expenses that distort budget reporting

- Missing documentation that triggers audit findings

These issues are far easier to resolve mid-month than during year-end close or an active audit.

In-House, Outsourced, or Automated: Choosing the Right AP Approach

Three Core Models

Each AP model comes with a different set of trade-offs. Here's how they compare at a glance:

| Model | Control | Speed to Deploy | Best For |

|---|---|---|---|

| In-House | Highest | Slow (hiring, training) | Stable teams with ERP expertise |

| Outsourced | Shared | Fast (immediate capacity) | Transitions, backlogs, lean teams |

| Automation | High (in-house) | Medium (integration needed) | Long-term efficiency at scale |

In-house AP keeps all functions internal, using your ERP and existing staff. It offers maximum control but requires adequate staffing, fund accounting knowledge, and ongoing training as regulations evolve.

Outsourced AP hands off some or all functions to an external partner who integrates with your ERP. It provides immediate capacity without hiring delays but demands careful vetting for data security and compliance fit.

AP automation software — tools like Bill.com, AvidXchange, or ERP-integrated modules — handles invoice capture, approval routing, and payment processing while keeping control in-house. The trade-off: upfront investment, staff adoption, and technical integration time.

When Outsourcing Makes Sense

Outsourcing delivers the greatest value for institutions managing system transitions, dealing with AP backlogs, experiencing staff turnover, or operating with lean finance teams. These situations require immediate capacity that can't wait for hiring cycles or system implementations.

Smaller colleges and community colleges, in particular, may benefit from boutique bookkeeping and consulting partners who can serve as an extended team without the overhead of large enterprise contracts. Sound Advice Bookkeeping, for instance, has worked with Worldmind — an outdoor-based educational organization — to establish accounting infrastructure and organize bookkeeping operations from the ground up. Their three-phase process (cleanup, discovery, and ongoing support) suits institutions that need to establish control quickly before transitioning to sustainable, long-term operations.

Trade-Offs to Consider

No single model is universally right. The practical considerations break down like this:

- Outsourcing: Fast to deploy and expertise-rich, but vendor fit matters — especially for data security and higher education compliance requirements

- Automation: Strong long-term ROI with full in-house control, but requires software investment, ERP integration, and staff buy-in before it pays off

- Hybrid: Often the most practical path for mid-sized institutions — outsource through crisis periods (migrations, backlogs, vacancies), then build toward in-house automation for the long run

How to Choose the Right AP Services Partner for Your Institution

Look for Higher Education Experience

Look for a partner who understands fund accounting, Uniform Guidance compliance (2 CFR Part 200), and the ERP systems common in academia—Banner, Workday, and Ellucian. They should also know the fiscal year rhythms of educational institutions: budget cycles, enrollment periods, and grant reporting deadlines.

Ask for references from comparable institutions and verify the partner has worked with educational clients facing similar challenges.

Evaluate Process for Compliance and Documentation

Confirm that any AP services partner can produce audit-ready records, support grant expenditure documentation, and align with your institution's internal controls and approval workflows. Ask specifically how they handle:

- Fund coding and allocation

- Three-way matching enforcement

- Documentation retention for federal grants

- IRS reporting for contractor payments

- Support during audits

A partner without this background typically slows your team down rather than freeing it up—errors in fund coding or grant documentation can surface months later during an audit.

Assess Scalability, Communication, and Fit

Capacity matters as much as capability. The right partner scales support during high-volume periods—year-end close, semester transitions, grant reporting deadlines—and communicates clearly about status, issues, and next steps.

A boutique partner that functions as an extension of your finance team often delivers more responsive service than a large generalist firm that treats your account as one of hundreds.

Chemistry matters—your AP partner will interact with department heads, vendors, and senior leadership. Choose a partner whose communication style and values align with your institutional culture.

Frequently Asked Questions

How much does it cost to outsource accounting?

Outsourced accounting costs vary based on scope, volume, and provider. Common models include per-invoice fees ($5–$15), monthly flat rates ($170–$2,000+), or hourly consulting ($85–$200+/hour). For higher education, those costs are typically offset by savings from reduced errors, avoided late fees, and prevention of audit findings.

Can accounts payable be done remotely?

Yes. AP can be fully managed remotely through cloud-based ERPs, digital invoice submission (email, vendor portals), and electronic payments (ACH, wire transfers). Many institutions now use remote or hybrid AP teams, particularly when working with outside AP partners. The tradeoff is straightforward: proper data security protocols in exchange for access to specialized expertise anywhere in the country.

What is the difference between AP outsourcing and AP automation for universities?

AP outsourcing means a third party handles AP tasks using their own tools, processes, and staff — you hand off responsibility and receive completed work. AP automation means the institution uses software to streamline its own internal processes (invoice capture, routing, approval, payment), maintaining control while improving efficiency. Some institutions use both: outsourcing through a crisis period while building in-house automation for the long term.

What compliance requirements affect accounts payable in higher education?

Higher education AP must comply with federal Uniform Guidance (2 CFR Part 200) for grant-funded purchases, state audit standards for publicly funded institutions, and IRS reporting rules for contractors (Form 1099-NEC for domestic vendors over $600, Form 1042-S for nonresident aliens). Each layer requires thorough documentation and accurate fund coding.

How long does it take to clean up a backlogged AP system at a university?

Timeline depends on backlog size and staff bandwidth. With experienced external AP professionals, significant cleanup often takes weeks to a few months. One documented university case study shows a backlog projected for six months completed in four by a dedicated team of six. Smaller institutions typically move even faster.

What are signs that a higher education institution needs outside AP help?

Watch for these warning signs:

- Invoice backlogs stretching beyond 30–60 days

- Frequent vendor complaints about late or untracked payments

- Audit findings tied to documentation gaps or weak internal controls

- Finance staff turnover leaving knowledge gaps

- A recent ERP migration that disrupted normal AP workflows

If your team is spending more time managing crises than processing invoices, outside help is worth considering.