Introduction

Too many small business owners run their companies straight from their checking account balance. When cash looks healthy, they spend; when it's low, they panic. This gut-based approach means flying blind—never knowing your true profit margins, missing tax deductions, or understanding where money actually goes.

Monthly bookkeeping solves this by building a disciplined rhythm: every 30 days, your transactions get recorded, categorized, and turned into reports that actually mean something. That clarity is what lets you stop guessing and start deciding—whether you can afford that new hire, that equipment purchase, or that next step in growth.

This guide covers what monthly bookkeeping actually includes in 2026 and what you can expect to pay—ranging from $200 to $1,000+ depending on complexity. You'll also learn how AI is reshaping the field, why human judgment still matters, and how to decide whether outsourcing or hiring in-house makes sense for your business.

Key Takeaways

- Monthly bookkeeping includes transaction categorization, bank reconciliation, and financial reports (P&L, Balance Sheet) delivered every month

- 2026 costs range from $200–$350/month for basic services to $1,000+ for businesses with payroll and multiple revenue streams

- AI automates data entry but can't replace human judgment for catching miscategorizations and edge cases

- Professional bookkeeping makes sense when you're behind on entries, guessing at cash flow, or dreading tax season

- Outsourced bookkeeping typically costs 40–70% less than hiring in-house for businesses under $10M revenue

What Does Monthly Bookkeeping Actually Include?

Monthly bookkeeping is the ongoing, recurring process of recording, categorizing, reconciling, and reporting your business's financial transactions. Unlike a one-time cleanup or year-end scramble, it's a consistent monthly rhythm that keeps your financial records current and accurate.

Transaction Categorization

Every month, each income and expense transaction flows through your accounting software and gets assigned to the correct category. Your $500 payment to a vendor might be categorized as "Office Supplies," while a client deposit goes into "Service Revenue." This categorization directly impacts your financial reports and tax deductions.

The catch? Automation makes mistakes. Bank feeds can miscategorize transactions based on ambiguous vendor names, frequently posting entries incorrectly. A loan payment might appear entirely as an expense instead of being split between principal (which reduces your liability) and interest (which is tax-deductible).

Personal contributions can also be miscategorized as revenue, artificially inflating your income and increasing your tax burden.

Human review catches what software misses. A skilled bookkeeper recognizes these patterns and corrects them before they distort your financial picture.

Account Reconciliation

Reconciliation matches your bookkeeping records against bank and credit card statements to verify every transaction is recorded correctly. This monthly process catches:

- Duplicate charges

- Missing transactions

- Data entry errors

- Fraudulent activity

Without monthly reconciliation, small discrepancies compound over time. You might think you have $10,000 in the bank when you actually have $7,500—a costly surprise when payroll comes due.

Reconciliation also matters for audit readiness. The IRS expects your books to match your bank statements. Skipping reconciliation creates cash-flow blind spots and makes it nearly impossible to defend your numbers during an audit.

Monthly Financial Reports

Standard monthly deliverables include:

- Profit & Loss Statement: Shows revenue minus expenses for the month — the real test of profitability, not just whether your bank balance went up. You might have $20,000 come in, but if you spent $25,000, you're down $5,000 regardless of your starting balance.

- Balance Sheet: Snapshots what you own (assets), what you owe (liabilities), and your equity at month-end, giving you a clear read on financial position and growth over time.

- Cash Flow Statement (optional): Tracks where cash actually moved, explaining why your profit figure doesn't always match your bank balance change — timing gaps from unpaid invoices, loan payments, and owner draws all play a role.

Add-On Services

Depending on your provider, monthly packages may include:

- Payroll processing and tax filing

- Accounts payable management (paying vendors)

- Accounts receivable management (collecting from clients)

- 1099 contractor tracking and filing

- Sales tax calculation and remittance

- Tax preparation support for quarterly estimates

Sound Advice Bookkeeping builds monthly packages around each business's specific needs, looking at your books through the lens of growth and efficiency — not just tax compliance. That means identifying operational patterns and cost-saving opportunities that a pure compliance approach tends to miss.

Monthly Bookkeeping Costs in 2026: What Small Businesses Should Expect

Monthly bookkeeping costs vary significantly based on your pricing model and business complexity. The three common structures are hourly billing, flat monthly fees, and project-based pricing.

Cost Tiers for 2026

- $200–$400/month (Basic): Transaction recording, expense categorization, and bank reconciliation for sole proprietors or single-member LLCs with under 100 monthly transactions

- $500–$1,500/month (Mid-Range): Multiple bank accounts, credit cards, basic payroll, and A/P or A/R management for businesses processing 100–500 transactions monthly

- $1,500–$3,500+/month (Premium): Multi-employee payroll, multi-entity structures, inventory management, and controller-level advisory for 500+ transactions per month

Key Cost Drivers

Several factors push your monthly rate higher or lower:

- Transaction volume — 50 transactions per month costs far less than 500; volume is the most direct pricing lever

- Entity type — S-Corps and partnerships run 30–50% more than sole proprietorships due to shareholder distributions, capital account tracking, and payroll entries

- Bookkeeper experience — certified professionals with specialized expertise charge more than entry-level processors; the premium buys error-catching and strategic insight

- Geographic location — relevant for in-house hires (San Francisco vs. rural Kansas), but virtual bookkeepers remove geographic cost variation entirely

- Scope — adding payroll, A/R collections, or advisory calls increases costs but expands what you get

In-House vs. Outsourced Costs

The 2024 median annual wage for U.S. bookkeepers is $49,210 ($23.66/hour). But that's just base salary.

Fully loaded costs—including employer payroll taxes (7.65% FICA minimum), benefits (typically 25–35% of salary), software licenses ($2,400–$6,000 annually), recruiting fees, and management overhead—push the real annual cost to $75,000–$95,000.

Outsourced bookkeeping for the same business typically runs $18,000–$60,000 annually, representing 40–70% savings. For businesses under $10M in revenue, outsourcing is almost always the more cost-effective choice.

| Revenue Band | In-House Annual Cost | Outsourced Annual Cost | Savings |

|---|---|---|---|

| $500K–$1M | $38,400–$48,000 | $6,000–$14,400 | 62-70% |

| $1M–$2M | $52,000–$65,000 | $12,000–$24,000 | 54-63% |

| $2M–$5M | $65,000–$85,000 | $24,000–$42,000 | 38-51% |

| $5M–$10M | $115,000–$165,000 | $42,000–$72,000 | 52-63% |

Why Flat-Fee Pricing Benefits Small Businesses

Flat-fee monthly models give you predictable budgeting — no surprise bills, no guessing what this month's invoice will look like.

Sound Advice Bookkeeping uses a customized flat fee determined through their 3-Phase Process: Phase 1 cleans up existing records, Phase 2 is a 3-month discovery period analyzing your transaction patterns, and Phase 3 establishes your flat monthly fee based on actual business needs. Pricing starts at $170/month and is based on transaction volume — not hours logged — so you pay for your actual complexity level, not arbitrary hourly estimates.

What's Changing in 2026: AI, Automation, and the Role of the Human Bookkeeper

AI-Powered Tools Streamline Routine Tasks

98% of accountants utilized AI and automation tools in the past year, primarily for data entry and transaction processing. Modern accounting software automatically:

- Categorizes transactions based on vendor patterns

- Syncs bank feeds in real-time

- Scans and extracts data from receipts using OCR

- Generates standard journal entries

- Matches payments to invoices

These tools cut manual data entry time significantly — tasks that used to consume a bookkeeper's afternoon now run in the background.

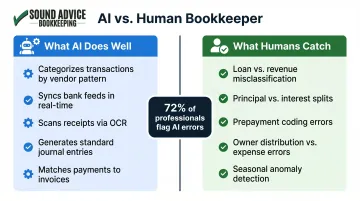

The Real Limitations of Automation

Software suggests categories but lacks context. AI doesn't know that:

- A $50,000 deposit was a business loan, not revenue

- A $3,200 payment splits between $3,000 principal and $200 interest

- A vendor payment was actually a prepayment for next quarter's services

- An owner withdrawal should be coded as a distribution, not an expense

72% of accounting professionals worry that AI could produce errors or incorrect decisions. These aren't unfounded concerns. Automated categorizations regularly miss nuances that impact your tax liability and financial accuracy.

Human bookkeepers catch what software misses — and those misses matter. A skilled bookkeeper will:

- Spot a sudden spike in "Office Supplies" that's actually miscategorized equipment

- Flag duplicate vendor payments before they become reconciliation headaches

- Recognize seasonal patterns and identify transactions that don't fit

Is AI Replacing Bookkeepers?

Not exactly — but it's changing the role. The BLS projects a 6% decline in traditional bookkeeping clerk jobs from 2024 to 2034 due to automation handling routine data entry. That's a shift in what the job looks like, not a disappearance of the profession.

The role is evolving from data entry clerk to financial analyst and advisor. As automation handles repetitive tasks, bookkeepers are taking on strategic responsibilities:

- Cash flow forecasting and planning

- Budget tracking and variance analysis

- Financial health assessments

- Process optimization recommendations

- Real-time financial insights for decision-making

85% of surveyed accounting practices now offer client advisory services, reflecting this shift. For small business owners, that means your bookkeeper in 2026 can do more than keep your records clean — they can help you make smarter decisions with the numbers in front of you.

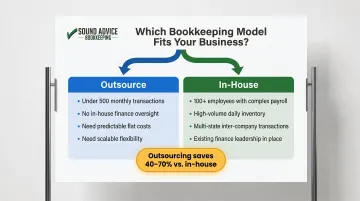

In-House vs. Outsourced Monthly Bookkeeping: Which Is Right for Your Business?

The Case for In-House Bookkeeping

Hiring an in-house bookkeeper makes sense when you need:

- An on-site bookkeeper who works exclusively on your business, understands your operations deeply, and is available for immediate questions

- High-volume daily inventory transactions, complex job costing, or multi-state payroll with union considerations — these often justify dedicated in-house staff

- Multi-entity operations with frequent inter-company transactions, where in-house coordination tends to be more efficient

The tradeoffs? Higher total costs (salary, benefits, payroll taxes, equipment, office space) and single-point-of-failure risk. When your bookkeeper takes vacation or calls in sick, your books stop. The average bookkeeper takes 20-25 business days off annually, leaving coverage gaps unless you cross-train other staff.

The Case for Outsourced Bookkeeping

Outsourcing typically works better for:

- Startups and growing small businesses that need professional bookkeeping without full-time overhead — 41% of professional services firms with $1M-$10M in revenue now outsource bookkeeping, up from 34% in 2023

- Businesses without a controller or CFO to oversee quality — outsourced firms include built-in multi-level review, team coverage, and no single point of failure

- Companies that need flexibility as they grow — outsourced services scale up or down without the cost and friction of hiring or letting go of full-time staff

Service level agreements typically guarantee books close within 10-15 days, regardless of individual schedules — something in-house arrangements rarely offer.

Quick Decision Framework

Use this as a quick gut-check before committing either way.

Consider outsourcing if you:

- Process fewer than 500 transactions monthly

- Lack in-house finance expertise to oversee bookkeeping quality

- Want predictable costs without benefits and payroll tax overhead

- Need flexibility to scale services as your business grows

Consider in-house if you:

- Employ 100+ people with complex daily payroll

- Manage high-volume inventory requiring daily reconciliation

- Operate multi-state locations with significant inter-company transactions

- Already have finance leadership to manage and oversee bookkeeping staff

Signs It's Time to Stop DIY-ing Your Books

Warning Signs You've Outgrown DIY Bookkeeping

Months of Missing Transactions: You're weeks or months behind on entry, and tax season becomes a reconstruction project instead of a planning opportunity.

Running on Bank Balance: Purchase decisions come down to what's in checking—not actual profitability. You could be cash-rich but losing money, or profitable but cash-poor due to timing gaps.

Tax Deadline Panic: Filing triggers stress because records are incomplete. Basic questions about income, deductions, or expense categories don't have quick answers.

60% of small business owners lack confidence in their accounting knowledge, and 45% report losing at least $10,000 in profits due to low financial literacy. DIY bookkeeping typically leads to missed deductions, miscalculated estimated taxes, uninformed spending, and no clear picture of where the business actually stands.

The Hidden Cost of DIY Bookkeeping

Time spent on bookkeeping is time not spent earning. For business owners billing $100–$300/hour, 10 hours a month on transaction entry means sacrificing $1,000–$3,000 in potential revenue.

DIY errors also compound quietly. Common problems include:

- Miscategorized payroll that distorts labor costs

- Loans recorded incorrectly, skewing liabilities

- Personal expenses mixed with business transactions

- Cleanup that costs far more than prevention would have

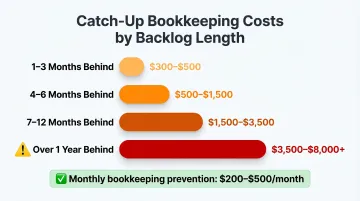

Catch-Up Bookkeeping Costs

Catch-up bookkeeping projects cost based on months of backlog:

- 1-3 months behind: $300-$500

- 4-6 months behind: $500-$1,500

- 7-12 months behind: $1,500-$3,500

- Over a year behind: $3,500-$8,000+

Staying current with monthly bookkeeping costs $200-$500/month. Letting it pile up for a year can cost $3,000+ to fix—plus the cost of poor decisions made without accurate financial data throughout that year.

Common Monthly Bookkeeping Mistakes Small Businesses Make

- Mixing personal and business expenses — a primary IRS audit trigger that makes it impossible to identify legitimate deductions

- Skipping small transactions — receipts under $75 and cash expenses seem minor, but the IRS requires documentation for all deductions and these gaps add up to thousands annually

- Skipping monthly reconciliation — leads to duplicate entries, missed income, and wrong account balances, so decisions get made on inaccurate data

- Getting reports but never reading them — financial statements only have value when you actually use them to spot trends and catch problems early

- Misclassifying employees as contractors — the liability here is severe; penalties for misclassification routinely exceed the payroll taxes the business was trying to avoid

Consistent process fixes all five of these. A dedicated bookkeeper builds a recurring monthly system around your business, so errors surface immediately instead of quietly compounding into a year-end disaster.

Frequently Asked Questions

How much should a monthly bookkeeper cost?

Monthly bookkeeping costs typically range from $200–$400 for basic services to $1,500–$3,500+ for full-service packages in 2026. The right cost depends on your transaction volume, business complexity, and whether you need add-ons like payroll or A/R management. Outsourced bookkeeping generally costs 40–70% less than hiring in-house.

What does monthly bookkeeping include?

Monthly bookkeeping includes transaction categorization, bank and credit card reconciliation, and financial reports (Profit & Loss and Balance Sheet). Depending on your provider, packages may also include payroll processing, accounts payable/receivable management, 1099 tracking, and tax preparation support.

Is AI replacing bookkeepers?

AI automates repetitive data entry and transaction categorization but cannot replace human judgment. Software regularly miscategorizes transactions — recording loans as revenue or splitting payments incorrectly. Human bookkeepers catch these errors, interpret complex transactions, and provide strategic insights that automation simply can't deliver.

What are the top 3 to 5 skills that make a great bookkeeper?

Great bookkeepers bring QuickBooks expertise, meticulous attention to detail, tax compliance knowledge, clear communication, and the pattern recognition to spot anomalies before they become problems. The strongest ones also connect financial data to business decisions — not just clean books for the tax man.

What is the best accounting software for startups?

QuickBooks Online, Xero, and FreshBooks are the most widely-used platforms for startups. QuickBooks leads with 62% market share; Xero suits collaborative teams with unlimited users at lower cost; FreshBooks works well for service businesses needing strong invoicing. Your bookkeeper's platform expertise often matters as much as the software itself.