Introduction

Small business owners often hit a jarring wake-up call when they start selling across state lines: the sudden realization that they may owe sales tax in states where they've never set foot, never opened an office, and perhaps never even visited. This isn't just a paperwork inconvenience—missed nexus obligations can trigger back taxes stretching years into the past, steep penalties that compound monthly, and audit exposure that can cripple a growing business.

The stakes are real. States have become aggressive in pursuing remote sellers since the 2018 South Dakota v. Wayfair Supreme Court ruling eliminated the physical presence requirement for sales tax collection. Today, crossing an economic threshold—often as low as $100,000 in annual sales to a state—creates the same tax obligations as opening a storefront there.

This guide breaks down the two concepts every multistate seller must understand: nexus (what triggers a tax obligation) and the step-by-step compliance process for registering, collecting, and filing once nexus is established. Whether you run an e-commerce store, a SaaS business, or a franchise operating across regions, here's how to get compliant and stay there.

Key Takeaways

- Nexus is the legal connection between your business and a state that creates a sales tax obligation—triggered by physical presence (office, employees, inventory) or economic activity (sales volume)

- The 2018 Wayfair ruling allows states to require sales tax collection based purely on sales volume, even without physical presence

- Most states use a $100,000 revenue threshold to define economic nexus; over 15 states have eliminated the 200-transaction test entirely

- Once nexus exists, you must register for a permit, collect the correct rate, and file on each state's schedule

- Organized records by state and transaction type are what make compliance provable in an audit

What Is Sales Tax Nexus?

Nexus is the legal connection between a business and a state that requires the business to collect and remit sales tax on sales made to customers in that state. There is no single federal standard—nexus is determined state by state, and the rules vary significantly.

The constitutional basis for nexus comes from the Commerce Clause (Article I, Section 8, Clause 3), which grants Congress authority over interstate commerce and restricts states from interfering with it. The Supreme Court evaluates whether a state tax is constitutional using the four-part Complete Auto Transit test, which requires that a tax applies to an activity with substantial nexus to the state, is fairly apportioned, doesn't discriminate against interstate commerce, and is fairly related to state services provided.

The Wayfair Decision Changed Everything

On June 21, 2018, the Supreme Court decided South Dakota v. Wayfair, Inc. in a 5–4 ruling that fundamentally altered sales tax nexus. The decision overturned the physical presence rule established in Quill Corp. v. North Dakota (1992) and National Bellas Hess (1967), ruling that physical presence is not necessary to establish substantial nexus. States can now mandate tax collection from out-of-state sellers based purely on economic activity.

What this means in practice: A small e-commerce business based in Colorado selling products to customers in 10 different states may now have nexus—and therefore tax obligations—in multiple states simultaneously, even if it has no employees, office, or warehouse in any of those states.

States wasted no time responding. Within a year, nearly every state with a sales tax had adopted laws to tax remote sales.

As of 2026, 45 states and the District of Columbia levy a statewide sales tax. Only five states do not: Alaska, Delaware, Montana, New Hampshire, and Oregon—though Alaska permits local municipal sales taxes.

Nexus catches many small and mid-sized businesses off guard. Any of the following can trigger obligations across multiple states without realizing it:

- E-commerce sellers shipping to customers nationwide

- Service businesses and SaaS providers with remote customers

- Businesses using third-party fulfillment networks like Amazon FBA

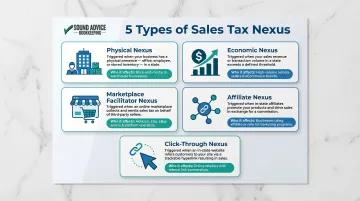

Physical Nexus vs. Economic Nexus: What's the Difference?

Physical Nexus

Physical nexus is a tangible, in-state presence that creates a tax obligation. Common triggers include:

- Office, store, or warehouse located in the state

- Employees working in the state, including remote workers based there

- Inventory stored in the state (including third-party warehouses or fulfillment centers)

- Company-owned vehicles making deliveries in the state

- Temporary presence such as attending trade shows or pop-up events

Concrete example: A Denver-based business with a remote employee working from Texas has established physical nexus in Texas and must comply with Texas sales tax rules, regardless of whether it has any other Texas connection.

Economic Nexus

Economic nexus is a threshold-based standard where sales activity—not physical presence—triggers a tax obligation. Following the Wayfair decision, all 45 states with a general sales tax have adopted economic nexus laws.

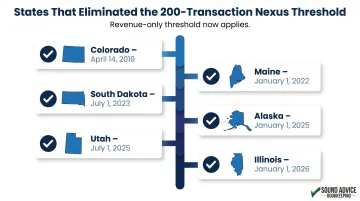

The most common threshold: The majority of states use $100,000 in gross receipts or 200 transactions in a year as the trigger. However, over 15 states have recently eliminated the 200-transaction threshold, relying solely on the revenue test to prevent disproportionate burdens on high-volume, low-dollar merchants.

States that removed the transaction count:

| State | Effective Date |

|---|---|

| Colorado | April 14, 2019 |

| Maine | January 1, 2022 |

| South Dakota | July 1, 2023 |

| Alaska | January 1, 2025 |

| Utah | July 1, 2025 |

| Illinois | January 1, 2026 |

Higher thresholds in major states:

- California: $500,000 in sales of tangible personal property

- New York: $500,000 in gross receipts AND 100 transactions (both thresholds must be met)

- Texas: $500,000 in gross revenue (including taxable, nontaxable, and exempt sales)

Other Nexus Types

Physical and economic nexus cover most situations — but three additional nexus types can catch businesses off guard, particularly those selling through online platforms or affiliate networks:

- Marketplace facilitator nexus: Amazon, Etsy, eBay, and similar platforms must collect and remit sales tax on third-party sales in all 45 states with a general sales tax — but your direct-sale obligations still apply separately.

- Affiliate nexus: Triggered when in-state affiliates or referral partners drive sales into a state on your behalf

- Click-through nexus: Applies when in-state residents earn commissions by referring customers to your online store, and those referrals exceed a state-set sales threshold

How to Determine Where You Owe Sales Tax

Step 1: Audit Your Business Footprint

Start by mapping out:

- All locations with physical presence: offices, remote employees, inventory storage (including third-party warehouses), and pop-up events

- Every state where you've made sales — pull data for the prior 12 months

- Gross receipts and transaction counts broken out by state

Without this data in hand, the threshold comparisons in Step 2 are guesswork.

Step 2: Compare Against State Thresholds

Once you have sales-by-state data, compare it against each state's published thresholds. A current state-by-state reference is available from the Streamlined Sales Tax Governing Board, which maintains up-to-date thresholds and rules.

Key considerations:

- Some states exclude exempt sales from threshold calculations

- Some use rolling 12-month periods instead of calendar years

- Thresholds must be re-evaluated regularly as states update rules

Step 3: Address Retroactive Exposure

If you've already crossed nexus thresholds in prior years without collecting tax, you may have a back-tax liability. Voluntary Disclosure Agreements (VDAs) offer a path to cure past non-compliance.

How VDAs work:

- The Multistate Tax Commission operates a program covering 38 participating states

- Taxpayers can apply anonymously until a VDA is signed

- States typically waive penalties and limit the lookback period to 3–4 years (instead of indefinite exposure)

- Prior contact from a state about a specific tax type disqualifies you from VDA participation for that state

Critical warning: If you trigger economic nexus but fail to register and file returns, the statute of limitations does not begin. States like Texas, Pennsylvania, and New York eliminate the lookback period entirely for failure to file or fraudulent returns, leaving businesses exposed to indefinite historical liability.

Step 4: Ongoing Monitoring

Nexus status is not a one-time determination. A business below the threshold today may cross it next quarter.

- Track cumulative sales by state throughout the year

- Flag when you're approaching thresholds (for example, at 80% of $100,000)

- Use accounting software or a compliance calendar to automate alerts

- Review nexus status at least quarterly

Register, Collect, and File: The Step-by-Step Process

Registration

Once nexus is confirmed in a state, you must obtain a sales tax permit from that state's department of revenue before collecting tax.

- Each state has its own registration process (most are online)

- You'll receive a state tax ID number required on all returns

- Do not begin collecting tax until you're properly registered—states like Colorado and Texas mandate registration prior to collection

Collection

After registration, configure your point-of-sale or e-commerce systems to apply the correct tax rate for each transaction.

Two areas trip up most businesses during collection:

- Tax rates vary by state, county, and municipality—not just by state

- ZIP codes are highly unreliable for tax calculation because a single 5-digit ZIP can contain multiple tax jurisdictions with different rates

- Use 9-digit ZIP codes or exact street addresses for accuracy

- Exemption certificates must be on file and valid before you skip collecting tax—if a customer claims an exemption and the certificate doesn't hold up, you're liable for the uncollected amount

In California, invalid resale certificates can trigger penalties of $500 or 10% of tax due per transaction. Keep your exemption records current and audit them regularly.

Filing

Filing frequency and deadlines are set by each state individually—and they vary widely.

Filing frequency examples:

- Colorado: Under $15/month collected = annual filing; under $600/month = quarterly; $600+ = monthly

- States assign frequencies based on your sales tax volume

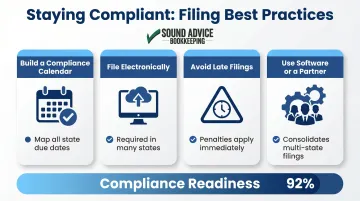

Once you know your frequencies, staying organized becomes the real challenge. These practices keep filings on track:

- Build a compliance calendar mapping every state's due dates

- File electronically where required (many states now mandate it)

- Late or inaccurate filings trigger penalties and interest—often with no grace period

- For businesses filing in multiple states, specialized software or a bookkeeping partner can consolidate the process significantly

Common Multistate Sales Tax Mistakes to Avoid

Assuming Physical Presence Is the Only Trigger

Many small business owners still operate under the pre-Wayfair assumption that if they don't have an office or employee in a state, they don't owe sales tax there. Economic nexus, click-through nexus, and marketplace nexus have made that assumption both outdated and expensive to hold onto.

These nexus types can create tax obligations in states where you've never set foot:

- Economic nexus: Triggered by sales volume or transaction count thresholds (typically $100,000 or 200 transactions)

- Click-through nexus: Applies when in-state affiliates or referral partners drive sales to your site

- Marketplace nexus: Covers sellers operating through platforms like Amazon, Etsy, or eBay

Ignoring Use Tax Obligations

Use tax applies when a business buys goods from a vendor who doesn't collect sales tax and then uses—rather than resells—those goods. The obligation falls on the buyer.

According to research on state tax compliance, use tax has the lowest compliance rate of any state tax—and it's one of the most common and expensive audit findings.

Common triggers:

- Promotional giveaways

- Inventory used internally

- Equipment purchases from out-of-state vendors

Relying on Inconsistent or Manual Processes

Inconsistent accounting practices are red flags for auditors: different workflows for different transaction sets, or records that can't be reconciled back to filed returns, signal weak internal controls.

What auditors look for:

- Documentation that clearly connects every filed return to underlying transaction data

- Records retained for the number of years each state's statute of limitations requires

- Consistent categorization and coding across all periods

In California, approximately 1% of active sales tax accounts are audited annually, resulting in over $626 million in deficiencies identified in FY 2023–2024. States increasingly use data analytics to flag high-risk accounts—late registrations after crossing economic nexus thresholds are a common targeting criterion.

When to Get Professional Help with Multistate Tax Compliance

Signs You've Outgrown DIY Compliance

- Filing in more than a handful of states

- Rapid revenue growth pushing you toward new nexus thresholds

- History of inconsistent record-keeping

- Discovery of unfiled back periods

- Receipt of an audit notice

At this point, the cost and risk of self-managing typically exceeds the cost of professional support. Five years after Wayfair, 72% of surveyed businesses agreed that online sales tax requirements remain complex and confusing.

If any of those signs apply, working with a bookkeeper who understands multistate compliance can prevent small oversights from becoming costly problems.

What Professional Help Looks Like

Sound Advice Bookkeeping works with small and mid-sized businesses across 30+ states, maintaining clean, audit-ready books that make sales tax compliance manageable and far less expensive when it matters most.

Services include:

- Auditing your business footprint to identify where sales tax obligations exist

- Structuring books by state and transaction type for clean, reviewable records

- Monitoring revenue by state to flag approaching nexus thresholds before you cross them

- Coordinating with State and Local Tax (SALT) specialists for filings and audit defense

- Organizing records needed to pursue Voluntary Disclosure Agreements (VDAs)

Proactive compliance means fewer surprises. When your books are organized by state and your thresholds are tracked, responding to a state notice becomes a manageable task rather than a crisis.

Frequently Asked Questions

What is multi-state sales tax?

Multi-state sales tax refers to the obligation a business has to collect, report, and remit sales tax in every state where it has established nexus. Nexus can be triggered by physical presence or by exceeding each state's economic nexus threshold.

What are tax compliance requirements for businesses selling in multiple states?

Core requirements include:

- Determining where nexus exists

- Registering for a sales tax permit in each applicable state

- Collecting the correct tax rate on taxable transactions

- Filing returns by each state's deadline

- Maintaining documentation to support all filings

How do I file sales tax in multiple states?

You must file a separate return in each state where you have nexus, according to that state's filing schedule (monthly, quarterly, or annually). Tax software or a professional service can centralize and automate much of this process.

What is nexus in sales tax, and how do I know if I have it?

Nexus is the connection that creates a sales tax obligation in a state. It's triggered by physical presence (employees, inventory, office) or by crossing that state's economic nexus threshold, commonly $100,000 in sales. Review your sales data by state at least quarterly.

What happens if I don't collect sales tax in a state where I have nexus?

Failure to collect and remit sales tax where nexus exists can result in back taxes, penalties reaching 25–50% depending on the state, and interest. Businesses that discover past non-compliance can often reduce penalties by applying for a Voluntary Disclosure Agreement before being audited.