Introduction

You spent years mastering clinical care, but running a medical practice also means running a business—and the financial side can quietly undo everything you've worked for. Many practice owners struggle with erratic cash flow, denied insurance claims, and tangled personal expenses, all while trying to serve patients. These aren't just bookkeeping headaches; they're threats to your practice's long-term survival.

Medical practice accounting goes far beyond basic bookkeeping. It involves insurance reimbursement cycles that can stretch 30–90 days, healthcare-specific compliance requirements under HIPAA and the False Claims Act, and cash flow gaps that general business accounting doesn't prepare you for.

According to the Healthcare Financial Management Association (HFMA), claim denial rates have climbed to nearly 12% in 2024, with private payers denying approximately 15% of claims on first submission. Each denied claim delays revenue and triggers rework, appeals, and compounding cash losses.

This guide walks through everything you need to build a financially sound practice: the accounting challenges specific to medical settings, how to set up a solid bookkeeping foundation, revenue cycle management, key financial statements and KPIs, tax-saving strategies, and the most costly mistakes to avoid.

Key Takeaways

- Medical practice accounting is more complex than standard business accounting due to insurance billing cycles, payer reimbursements, and healthcare regulations

- Every practice needs a proper bookkeeping system, a healthcare-tailored chart of accounts, and clean separation of personal and business finances

- Poor revenue cycle management (RCM) is the fastest path to denied claims and cash flow gaps — getting RCM right is non-negotiable for a healthy practice

- Track three core financial statements monthly plus key KPIs like AR days and claim denial rate

- Tax strategies like Section 179 deductions and retirement plans can meaningfully cut your practice's tax bill — but only if you're using them

What Makes Medical Practice Accounting Uniquely Complex

Unlike most businesses that receive payment at the point of sale, medical practices often wait 30–90 days for reimbursement from insurers—sometimes longer. This structural delay creates cash flow challenges that standard accounting methods don't address well. Medicare pays all clean claims within 30 days of receipt and owes providers interest on any late payments, but "clean" is the operative word.

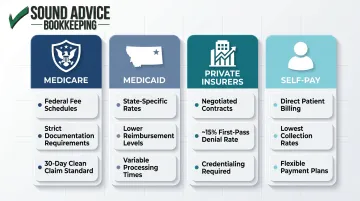

The Payer Mix Reality

Most clinics receive payment from a combination of sources, each with different rules:

- Medicare – Federal fee schedules, strict documentation requirements, 30-day clean claim standard

- Medicaid – State-specific rates, often lower reimbursement, variable processing times

- Private insurers – Negotiated contracts, varying fee schedules, higher denial rates (~15% first-pass)

- Self-pay patients – Direct billing, lowest collection rates, payment plan management

Each payer requires separate tracking for billing codes, reimbursement rates, and claim status. You can't manage cash flow without knowing which bucket each dollar falls into.

Accrual vs. Cash Accounting

Most medical practices should use accrual accounting, which records revenue when services are rendered—not when payment arrives. This method provides a realistic picture of what you've earned, even if cash hasn't hit the bank yet.

Here's how the two methods compare in practice:

| Method | Revenue Recorded When... | Best For |

|---|---|---|

| Accrual | Service is rendered | Most practices with insurance billing |

| Cash | Payment is received | Solo/micro practices, minimal insurance |

The IRS permits small businesses and qualified personal service corporations to use the cash method if average annual gross receipts are $32 million or less (2026 threshold). For solo practices with minimal insurance billing, cash accounting may work—but as volume grows, accrual gives you the visibility you actually need.

HIPAA's Indirect Impact

Financial data tied to patient records falls under HIPAA's reach. If your bookkeeper or external accountant accesses protected health information (PHI), they qualify as a Business Associate under HHS regulations and must sign a Business Associate Agreement (BAA). Skipping this step isn't a technicality—HHS can impose penalties ranging from $100 to $50,000 per violation depending on the level of negligence.

The Compliance Layer

Healthcare billing carries unique legal risks:

- False Claims Act (FCA) – The civil FCA defines "knowing" to include not only actual knowledge but also deliberate ignorance or reckless disregard of truth or falsity. Penalties include fines up to three times the programs' loss plus per-claim penalties.

- Insurance-specific documentation requirements – Every billed service must be supported by documentation that justifies the level of care and billing code used.

- Audit risk – Incorrect coding or inadequate documentation can trigger audits from Medicare, Medicaid, or private payers, leading to clawbacks and penalties.

For these reasons, your chart of accounts, billing records, and supporting documentation need to stay in sync—not just for financial clarity, but because they may be reviewed by a federal auditor.

Building Your Medical Practice Bookkeeping System

Separate Business and Personal Finances

Set up a dedicated business bank account and credit card exclusively for the practice. Mixing personal and business finances is one of the most common and damaging mistakes medical practice owners make. Even occasional personal charges on a business account create tax liability confusion, complicate bookkeeping, and raise red flags in an audit.

Open separate accounts the day you start your practice and keep them strictly separate from day one.

Create a Healthcare-Specific Chart of Accounts

Your chart of accounts is the framework for all financial tracking. A medical practice needs categories that reflect healthcare operations:

Revenue accounts:

- Patient revenue by service type (office visits, procedures, lab work, telehealth)

- Insurance receivables by payer type

Asset accounts:

- Accounts receivable (aging by payer)

- Medical equipment and furniture

- Inventory (clinical supplies, pharmaceuticals)

Expense accounts:

- Payroll and staff costs (clinical and administrative)

- Clinical supplies and disposables

- Medical equipment maintenance and depreciation

- Rent and utilities

- Malpractice insurance

- Professional development and CME

- Billing and coding services

- IT and practice management software

A well-designed chart of accounts enables you to track profitability by service line, compare costs against benchmarks, and make informed pricing and staffing decisions.

Establish Core Bookkeeping Processes

Three processes must run consistently:

Categorization – Record and label every transaction accurately. Each insurance payment, supply purchase, and payroll run gets coded to the correct account.

Reconciliation – Match your books to bank statements and insurance remittance reports monthly. This catches errors, identifies missing payments, and ensures your records reflect reality.

Reporting – Generate financial statements for regular review. Without them, cash flow gaps and claim denials go undetected until they become real problems.

Choose the Right Accounting Platform

QuickBooks (Online, Desktop, or Enterprise) is the most widely used accounting platform for small medical practices. It offers flexibility, report customization, and broad professional support. However, QuickBooks alone isn't enough. You'll also need integration with a HIPAA-compliant practice management system for patient-linked financial data.

Setting up QuickBooks correctly for a medical practice requires expertise in healthcare accounting. Working with a bookkeeper who has deep QuickBooks expertise, like the team at Sound Advice Bookkeeping, can fast-track a proper, growth-oriented setup tailored to your practice's specific needs.

Update Frequently

Books should be updated weekly at minimum, not just at tax time. Delayed recording leads to:

- Missing transactions that never get entered

- Incorrect reimbursement tracking

- Poor cash flow visibility

- Inability to catch denied claims quickly

- Decisions made based on checking account balance instead of actual financial position

For medical practices, where insurance reimbursements can lag weeks behind service delivery, weekly updates are the difference between knowing your real financial position and guessing at it.

Revenue Cycle Management: Tracking Every Dollar You've Earned

Revenue cycle management (RCM) covers the full process — from patient scheduling and insurance verification through charge entry, claims submission, payment posting, and final collections. Each step carries accounting implications, and a breakdown anywhere in the cycle means lost revenue.

Understanding how to track and tighten each stage is what separates practices that grow from those that constantly chase cash.

Accounts Receivable Management

Every unpaid insurance claim or patient balance is an asset on your books until collected. Track AR aging reports that segment outstanding balances by time period: 0-30 days, 31-60 days, 61-90 days, and 90+ days. The longer a claim sits unpaid, the less likely you are to collect.

MGMA benchmarks indicate optimal Days in A/R is 30-40 days, with a clean claims rate of 98% and net collection rate of 97% to 99%. If your Days in A/R consistently exceeds 40, you have a revenue cycle problem that's steadily draining your cash reserves.

Denial Management

When an insurer rejects a claim, you must appeal promptly. MGMA's 2023 DataDive shows an 8% first-submission denial rate for single-specialty groups, but rates vary by payer. Medicare Advantage presents particular challenges: a Health Affairs study found 17.7% of initial MA claims were denied, and while 57% of all claim denials were ultimately overturned, denials still resulted in a 7% net reduction in provider revenue.

Those numbers make one thing clear: every denied claim that isn't appealed is revenue lost permanently. Build a denial tracking system that logs reason codes, assigns responsibility for appeals, and monitors resolution rates.

Key RCM Metrics

Monitor these metrics monthly:

- Days in AR – Time between service delivery and payment receipt (target: 30-40 days)

- Collection rate – Percentage of billed charges actually collected (target: 97-99%)

- First-pass claim acceptance rate – Percentage of claims paid without resubmission or appeal (target: 98%)

- Denial rate – Percentage of claims denied on first submission (benchmark: 8-12%)

Automate Patient Payment Processes

Reducing friction in the payment process directly accelerates collections. Set up automated reminders for outstanding patient balances and give patients multiple ways to pay:

- Automated reminders at 30, 60, and 90 days post-service

- Online patient portals for 24/7 self-service payment

- Credit card and ACH payment acceptance

- Structured payment plans for larger balances

The fewer barriers between a patient and their "pay now" button, the faster money hits your account.

Financial Statements and KPIs Every Practice Should Monitor Monthly

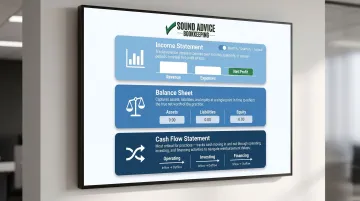

The Three Essential Statements

Income Statement (Profit & Loss): Shows revenue vs. expenses over a period (typically monthly, quarterly, or annually). This tells you whether your practice made or lost money and where expenses are concentrated.

Balance Sheet: Shows assets, liabilities, and equity at a specific point in time. This reveals your practice's financial position: what you own, what you owe, and your net worth.

Cash Flow Statement: Shows actual cash moving in and out through operating, investing, and financing activities. This is the most important statement for medical practices — insurance reimbursement delays mean you can be profitable on paper while running out of cash.

Together, these three statements give you the full picture — and the KPIs below tell you whether the numbers inside them are trending in the right direction.

Key Financial KPIs for Medical Practices

| KPI | Definition | Target | What It Indicates |

|---|---|---|---|

| Days in AR | Current receivables divided by average daily charge amount | 30-40 days | How quickly you're collecting payments; lower is better |

| Claim Denial Rate | Claims denied on first submission divided by total claims submitted | 8-12% (industry avg); target <5% | Quality of billing and coding processes |

| Operating Profit Margin | Net income divided by gross revenue × 100 | 15-25% (varies by specialty) | Pricing efficiency and cost control |

| Days Cash on Hand | Current cash and cash equivalents divided by average daily operating expenses | 30-60 days minimum | How long you could operate on current cash reserves |

Review these metrics monthly and compare month-over-month and year-over-year trends. Rising bad debt, declining margins, or lengthening Days in AR are early warning signs that allow you to act before they compound into larger revenue losses.

Tax Strategies That Save Medical Practices Real Money

Section 179 Depreciation

Medical equipment—diagnostic tools, computers, office furniture, ultrasound machines—can often be fully deducted in the year of purchase rather than depreciated over multiple years. For 2025, the Section 179 maximum deduction is $2,500,000, with a phase-out threshold of $4,000,000. If you purchase under $4 million in qualifying property, you can deduct up to $2.5 million immediately.

That's a direct boost to cash flow. If equipment purchases are on your roadmap, timing them strategically can create meaningful deductions — and retirement accounts offer another layer of tax relief on top of that.

Retirement Plan Contribution Strategies

Self-employed physicians and practice owners can contribute significantly more to retirement accounts than employees, reducing current taxable income while building long-term wealth:

- SEP-IRA — Contribute the lesser of 25% of compensation or $70,000 for 2025. Low administrative overhead, easy to establish.

- Solo 401(k) — Combines employee deferrals ($23,500 for 2025) with employer profit-sharing, up to $70,000 total ($77,500 if age 50+).

- Defined Benefit Plan — For high earners, these often allow contributions exceeding $200,000 annually, calculated by an actuary based on your income and age. The 2025 annual benefit limit is $280,000.

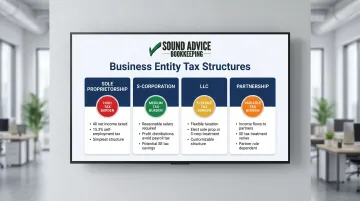

Entity Structure Matters

Whether you operate as a sole proprietorship, S-corp, LLC, or partnership affects self-employment taxes, pass-through income, and overall tax liability. Each structure carries different tax implications:

- Sole Proprietorship — All net income subject to self-employment tax (15.3%)

- S-Corp — Pay yourself a reasonable salary; remaining profits taken as distributions avoid payroll tax

- LLC — Flexible; taxed as sole proprietorship or S-corp depending on elections made

- Partnership — Income flows through to partners; structure affects how SE taxes apply

A tax professional familiar with medical practice structures can identify which entity saves the most given your income level and long-term goals.

Common Accounting Mistakes Medical Practices Make

Mixing Personal and Business Finances

Using your business account for personal expenses—or vice versa—creates tax liability confusion, complicates bookkeeping, and raises red flags during audits. The IRS can disallow business deductions if they determine you aren't maintaining proper separation.

The fix: Use separate accounts exclusively and transfer funds between accounts only as formal owner draws or capital contributions. Never pay personal expenses directly from business accounts.

Neglecting Revenue Cycle Follow-Up

Unpursued denied claims and untracked patient balances lead to silent revenue leakage. It doesn't show up as an obvious problem until margins are already suffering. Industry data shows about 40% of claims are paid with no human intervention, leaving 60% that require some level of follow-up, correction, or appeal.

The fix: Implement systematic AR aging review, denial tracking, and patient balance follow-up processes. Assign clear responsibility and monitor resolution rates weekly.

Waiting Until Tax Season to Review Books

Reactive bookkeeping means missing mid-year opportunities to course-correct on spending, reimbursement rates, or cash reserves. You can't adjust what you don't measure, and you can't measure what isn't recorded.

The fix: Review financial statements monthly. A monthly bookkeeping partner—like Sound Advice Bookkeeping—keeps your records current year-round, so you're never scrambling for year-end cleanup or making decisions on stale numbers.

Frequently Asked Questions

What is the difference between cash and accrual accounting for a medical practice?

Cash accounting records revenue only when payment is received, which is simple but creates blind spots in a billing-heavy environment. Accrual accounting records revenue when services are rendered — a better fit for clinics managing insurance reimbursements and needing a realistic picture of earnings.

What bookkeeping software is best for small medical practices?

QuickBooks (Online or Desktop) is the most widely used option for small practices due to its flexibility and broad professional support. Pair it with a HIPAA-compliant practice management system for patient-linked financial data, as QuickBooks alone doesn't meet healthcare privacy requirements.

How often should a medical practice reconcile its accounts?

Reconcile bank and insurance accounts monthly at minimum. For higher-volume payers, weekly or biweekly reconciliation catches errors and denied claims before they pile up into larger cash flow problems.

What are the biggest tax deductions available to private medical practices?

The highest-impact deductions for private practices include:

- Section 179 equipment deductions — up to $2.5 million for 2025

- Retirement plan contributions — SEP-IRA, Solo 401k, or defined benefit plans

- CME and professional development expenses

- Home office or clinical space deductions

When should a medical clinic consider outsourcing its bookkeeping?

Consider outsourcing when practice volume outpaces what you can track accurately, claim denials are rising without clear explanation, or you're making financial decisions based on your checking account balance instead of actual reports.

What financial KPIs should a private practice track every month?

The top four are Days in AR (target 30-40 days), claim denial rate (target below 8%), operating profit margin (typically 15-25%), and days cash on hand (minimum 30-60 days). These provide early warning signs before financial problems become crises.