Introduction

Strong sales shouldn't mean cash flow stress — but for many small business owners, that's exactly what happens. When invoices sit unpaid for 30, 60, or even 90 days, your business is essentially extending interest-free loans to customers while you scramble to cover payroll, rent, and vendor bills.

Accounts receivable (AR) services close that gap by turning outstanding invoices into predictable cash flow. This guide covers the role of AR in small business finances, common management challenges, core best practices — including payment terms and the 5 C's credit framework — and when outsourcing AR becomes the smarter choice.

Key Takeaways

- AR represents money customers owe you for delivered goods or services—managing it well is essential for steady cash flow

- Small businesses most often fall behind on invoicing, follow-up, and tracking which receivables are overdue

- Effective AR includes clear payment terms, automated reminders, weekly aging report reviews, and early-pay incentives

- Payment terms (Net 30/60/90) and the 5 C's framework guide smarter credit decisions before problems start

- When AR becomes unmanageable in-house, outsourcing reduces time spent chasing payments and improves financial predictability

What Are Accounts Receivable Services and Why Do They Matter?

Accounts receivable represents outstanding invoices or money owed to your business by customers for products or services delivered on credit. AR sits on your balance sheet as a current asset and reflects expected revenue—but only if you actually collect it.

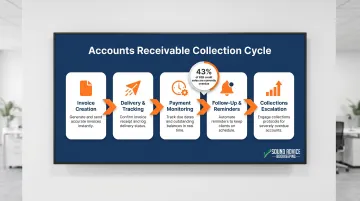

AR services encompass the full collection cycle:

- Invoice creation and delivery

- Payment tracking and status monitoring

- Follow-up communications and collections

- Aging report generation and analysis

- Customer payment coordination

These managed services differ fundamentally from accounting software alone. QuickBooks can track invoices, but it can't make phone calls, send strategic reminders, or escalate delinquent accounts. Professional AR services close that gap, pairing software automation with human follow-through to move unpaid invoices toward actual payment.

Without active management, high AR balances quickly signal collection problems. 43% of US B2B credit sales are currently overdue, which means nearly half of all invoiced revenue is sitting unpaid at any given time. Well-managed AR provides visibility into cash flow timing, customer payment behavior, and your actual capacity for growth.

Why Small Businesses Struggle with Accounts Receivable

Small businesses face three core AR challenges that compound cash flow stress:

Manual or Inconsistent Invoicing Processes

Without automated systems, invoicing happens irregularly—often days or weeks after work is completed. This delay pushes payment timelines even further out. Lean teams juggle multiple responsibilities, and billing gets deprioritized when more urgent tasks arise.

Delayed Follow-Up Due to Bandwidth Constraints

Most small business owners lack dedicated accounting staff. When invoices go unpaid, follow-up falls to whoever has time—which often means no one. A 30-day invoice becomes 60 days, then 90, then effectively uncollectible. Recovery probability drops to 69.6% at 90 days and plummets to just 22.8% after one year.

No Formal Collections Policy

Without written procedures for escalation—second invoices, phone calls, late fees—collection efforts are reactive and inconsistent. Customers learn that payment deadlines are flexible, which encourages slower payment behavior.

Poor AR visibility leads to reactive financial management. When you don't know which invoices are 30, 60, or 90+ days overdue, cash flow projections become guesswork. That uncertainty ripples into every business decision:

- Hiring and staffing choices

- Inventory and supply purchases

- Equipment investments

- Growth and expansion opportunities

Many small business owners avoid following up on overdue invoices, worried it will strain client relationships. Professional, systematic AR follow-up actually protects those relationships. Customers respect clear expectations and consistent processes—what damages relationships is the awkward, reactive outreach that happens after invoices have aged past 90 days.

How to Manage Accounts Receivable Effectively: Core Practices for Small Businesses

Set Clear, Written Payment Terms Upfront

Every client engagement should include written payment terms covering:

- Due dates (Net 30, Net 60, etc.)

- Accepted payment methods (ACH, check, credit card)

- Late fees (e.g., 1.5% per month on balances over 30 days)

- Early-pay discounts (e.g., 2% off for payment within 10 days)

Ambiguity in payment expectations is one of the top reasons invoices go unpaid. When terms are vague, customers default to paying on their schedule, not yours.

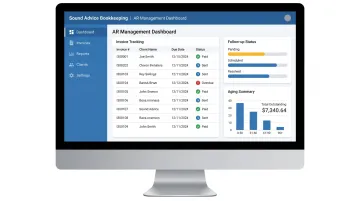

Automate Your Invoicing and Reminder System

QuickBooks and similar platforms allow you to:

- Schedule invoices to send automatically on project completion or monthly cycles

- Send automated reminders 3 days before due date, on due date, and at 7/15/30-day intervals after

- Track payment status in real time with dashboard visibility

Sound Advice Bookkeeping handles this QuickBooks configuration as part of their Phase 1 setup — so invoicing workflows and reminder sequences are built correctly from the start, not patched in later.

Implement an Aging Report Review Cadence

Once your automation is running, your aging report tells you what it's catching — and what still needs your attention. It breaks outstanding invoices into time buckets:

- 0-30 days (current)

- 31-60 days (attention needed)

- 61-90 days (urgent)

- 90+ days (critical/collection risk)

Review aging reports weekly or bi-weekly. At each stage, take specific action:

- 0-30 days: Send friendly payment reminder

- 31-60 days: Follow up with email and phone call

- 61-90 days: Issue formal past-due notice with late fees

- 90+ days: Escalate to collections partner or legal demand

Offer Structured Incentives and Consequences

Balance encouragement with enforcement:

- Early payment discounts: Offer 1-2% off the invoice total for payment within 10 days — gets money in the door faster and rewards prompt clients.

- Late payment fees: Charge 1.5-2% monthly interest on balances past 30 days. Put this in writing upfront and apply it uniformly.

Both policies only work if you enforce them consistently. Selective application creates confusion and quietly trains clients to ignore your terms.

Know When to Escalate

Establish a clear escalation path:

- Email reminders (automated)

- Personal phone calls (at 30 and 60 days)

- Formal demand letter (at 90 days)

- Third-party collection partner (at 120+ days)

How fast you escalate determines how much you recover. Companies write off up to 5% of long-overdue invoices as bad debt, with collection probability dropping significantly past 90 days. Waiting costs you money.

Understanding Payment Terms and the 5 C's of AR Management

Net 30, Net 60, Net 90 Payment Terms Explained

These terms indicate when payment is due after the invoice date:

- Net 30: Payment due within 30 days

- Net 60: Payment due within 60 days

- Net 90: Payment due within 90 days

Industry norms vary. Professional services typically use Net 30, while construction and manufacturing may extend Net 60 or Net 90 to align with project timelines.

Extended terms affect working capital. If you offer Net 60 terms but have Net 30 payment obligations to vendors, you create a 30-day cash flow gap that must be covered from reserves or credit lines.

When longer terms make sense:

- Landing large contracts where competitors offer extended terms

- Serving industries with standard longer payment cycles

- When you have sufficient cash reserves to absorb the delay

When to avoid longer terms:

- Your business operates on tight margins with limited reserves

- Customer creditworthiness is uncertain

- You're experiencing cash flow constraints

The 5 C's of Accounts Receivable Management

The 5 C's framework helps evaluate client credit risk before extending payment terms:

1. Character: Payment history and vendor reputation — check references and research how reliably they pay.

2. Capacity: Ability to pay based on revenue and cash flow. Does the client generate enough income to cover your invoice without strain?

3. Capital: Overall financial strength, including balance sheet health, existing debt, and liquidity.

4. Collateral: Assets that back the obligation. For larger contracts, know what the client could liquidate if payments stall.

5. Conditions: Industry trends, economic climate, and seasonal factors that affect whether payment is likely to arrive on time.

Using the 5 C's Practically Before Extending Credit

Before approving terms for a new client, gather the basics:

- Business references (2-3 vendors or clients)

- Credit check (through Dun & Bradstreet or a similar service)

- Years in business and ownership stability

- Annual revenue estimates

- Industry and market conditions

Once you have that picture, use it to set appropriate terms. A simple risk-to-terms framework:

| Risk Profile | Signal | Recommended Terms |

|---|---|---|

| High risk | Weak character + limited capacity | 50% deposit or Net 15 |

| Moderate risk | Good character + moderate capacity | Net 30 standard terms |

| Low risk | Excellent character + strong capacity | Net 60 or early-pay discount |

A few hard-and-fast thresholds worth building into your policy:

- New businesses (< 2 years): Require 50% deposit upfront

- Poor payment history with other vendors: Cash on delivery (COD)

- Strong financials + excellent references: Extended terms acceptable

Payment Terms and Days Sales Outstanding (DSO)

Days Sales Outstanding measures the average number of days it takes to collect payment after a sale. Calculate DSO as:

DSO = (Accounts Receivable ÷ Total Credit Sales) × Number of Days

For small businesses, healthy DSO typically ranges from 30-45 days. Longer payment terms inflate DSO—offering Net 60 terms will naturally push DSO toward 60+ days.

DSO as a performance metric:

- DSO trending upward: Collection efforts are weakening

- DSO trending downward: Collection efficiency is improving

- DSO above 60 days: Urgent review needed

Ongoing Credit Risk Management

Don't treat credit risk as a one-time check at onboarding. A client's financial position and market conditions can shift, turning a reliable payer into a collection problem. Reassess credit risk:

- Annually for all clients

- When payment patterns change (late payments increase)

- During major economic shifts or industry disruptions

- Before extending larger contracts or credit limits

When to Outsource AR Services—and What to Look For

Signs AR Management Has Outgrown In-House Capacity

Self-assessment checklist:

- Your DSO consistently exceeds 45-50 days

- More than 20% of invoices regularly age past 60 days

- You spend 5+ hours weekly chasing payments

- No one reviews aging reports consistently

- You lack formal follow-up procedures

- Cash flow unpredictability limits business decisions

- Customer follow-up feels awkward or gets delayed

If you checked three or more items, outsourcing AR likely makes financial sense.

Core Benefits of Outsourcing AR Services

Faster invoicing cycles: Professional AR teams invoice immediately upon project completion, reducing the delay between delivery and payment request.

Professional collections follow-up: Systematic reminders and escalation preserve client relationships better than inconsistent personal outreach. Customers respond more professionally to structured processes.

Access to reporting and visibility: Outsourced AR providers deliver weekly or monthly aging reports, DSO tracking, and collection performance metrics without requiring dedicated accounting staff.

Scalable processes: As your business grows, AR services scale with transaction volume rather than requiring additional hires.

What to Look For in an AR Services Partner

Knowing the benefits is one thing — finding the right partner to deliver them is another. Here's what actually separates a good AR services provider from a generic one:

- QuickBooks integration: Your AR partner should connect directly to your accounting system. QuickBooks dominates small business accounting, so confirm compatibility before signing anything.

- Flat-fee pricing: Avoid providers that charge per transaction or tack on fees for follow-up calls and letters. Flat-fee structures based on transaction volume are easier to budget and harder to game.

- Your brand voice, not theirs: AR follow-up should sound like it's coming from your business. The right provider adapts their tone and messaging to fit your client relationships — not a generic collections script.

- Scalable tiers: Look for a partner who can handle more volume as you grow, without forcing you into a full renegotiation every time your business changes.

- Cash flow context: Aging reports matter, but the best providers connect AR performance to cash flow forecasting — giving you a fuller picture of financial health, not just a list of overdue invoices.

Sound Advice Bookkeeping integrates AR management into monthly bookkeeping packages starting at $170/month. Their process includes issuing second invoices, making follow-up calls, and implementing escalation steps at 30, 60, and 90-day intervals — all while maintaining your brand voice and protecting your client relationships.

AR Services vs. Debt Collectors: The Critical Difference

Many business owners confuse AR services with debt collection agencies. The difference matters:

AR services manage your receivables proactively as an ongoing business function. They handle invoicing, tracking, and systematic follow-up to ensure invoices are paid on time—ideally before they reach 60 or 90 days past due.

Debt collection agencies are engaged reactively after accounts have already defaulted. They pursue invoices that have aged past 90-120 days and are considered uncollectible through normal business channels.

Professional AR management is designed to prevent the need for collections. By maintaining consistent follow-up and escalation processes, AR services keep most invoices from ever reaching the default stage.

Frequently Asked Questions

What are accounts receivable services?

AR services manage the full cycle of invoicing, payment tracking, follow-up, and collections on behalf of a business. They ensure timely payments and steady cash flow by handling tasks most small business owners lack time to manage consistently.

How do you manage accounts receivable for a small business?

Set clear payment terms upfront, automate invoicing and reminders through QuickBooks or similar software, and review aging reports weekly. Follow up at 30/60/90-day intervals and escalate overdue accounts on a defined schedule — businesses that skip this structure are the ones most likely to write off bad debt.

How do you effectively collect accounts receivable?

Invoice promptly after delivery, implement structured follow-up sequences at 30/60/90-day intervals, and offer payment flexibility when needed. Escalate to a collections partner only after internal efforts are exhausted — collection rates drop sharply after 90 days, so early action matters.

Are accounts receivable services debt collectors?

No. AR services are proactive, ongoing financial management functions that prevent accounts from becoming delinquent. Debt collectors are reactive third parties engaged after accounts default. The goal of AR services is to collect before escalation becomes necessary.

What are 30-60-90 payment terms?

These refer to Net 30, Net 60, and Net 90 terms—meaning payment is due 30, 60, or 90 days from the invoice date. Longer terms require stronger cash reserves or active AR management to avoid cash flow gaps.

What are the 5 C's of accounts receivable management?

Character, Capacity, Capital, Collateral, and Conditions are a credit evaluation framework used before extending payment terms. Character refers to a client's payment history; Capacity measures their ability to pay; Capital, Collateral, and Conditions assess financial backing and business environment. Running through this framework before offering Net 30 or longer terms helps small businesses avoid extending credit to high-risk customers.